Serious writing for

serious readers

Summary

4 November 2013

Most of my writings on Islamic finance are written to discuss specific points such as how it should be taxed, regulated or accounted for. According they are written in a style suitable for their intended audience, which is people who are already familiar with Islamic finance but want to explore detailed aspects.

However a few years ago a newspaper article led me to write "A simple introduction to Islamic mortgages."

Sukuk have recently had a significant amount of UK press coverage following David Cameron's speech on the opening day of the World Islamic Economic Forum in London, 29 October 2013. He said:

This government wants Britain to become the first sovereign outside the Islamic world to issue an Islamic bond.

So the Treasury is working on the practicalities of issuing a bond-like sukuk worth around £200 million and we very much welcome the involvement of industry in developing this initiative which we hope to launch as early as next year.

The Prime Minister also talked about the Government's commitment to a strong financial services industry in London, and how the UK welcomes investment from all sources. It is worth reading the full text of the Prime Minister's speech.

Since then, many people have asked me "What is a Sovereign sukuk?" Very briefly, a sukuk is an Islamic finance instrument which is analogous to a tradable bond. A sovereign sukuk is one issued on behalf of a sovereign entity.

In finance, a bond is an instrument which acknowledges a debt. For example, XYZ plc may borrow £1 million from investors, and issue the investors 1,000 bonds each of which has a denomination of £1,000 to acknowledge that XYZ plc owes £1,000 on that bond. The bonds may be in the form of a paper certificate, but today are more likely to exist only in electronic form, held in the records of a registration agent.

Each £1,000 bond will set out its terms, such as:

Such bonds are not permissible in Islamic finance as they involve the payment and receipt of interest.

Sukuk is an Arabic word which is the plural of sakk which means certificate and is the source of the English word cheque. In English the word sukuk is uniplural, so "one sukuk", "two sukuk" etc.

Sukuk in their modern Islamic finance form were invented in Malaysia around the year 2000. They are designed to have economic implications for the issuer and the investor which are essentially similar to tradable bonds, but without having any interest paid or received. That means that there can be no legal debt involved.

The goal is to design an instrument which can be bought and sold between different holders, provides finance for a fixed period of time, typically three to five years although longer periods of time are used, and from the perspective of investors, provides a flow of regular payments which has priority over the payment of rewards to ordinary shareholders, without involving interest.

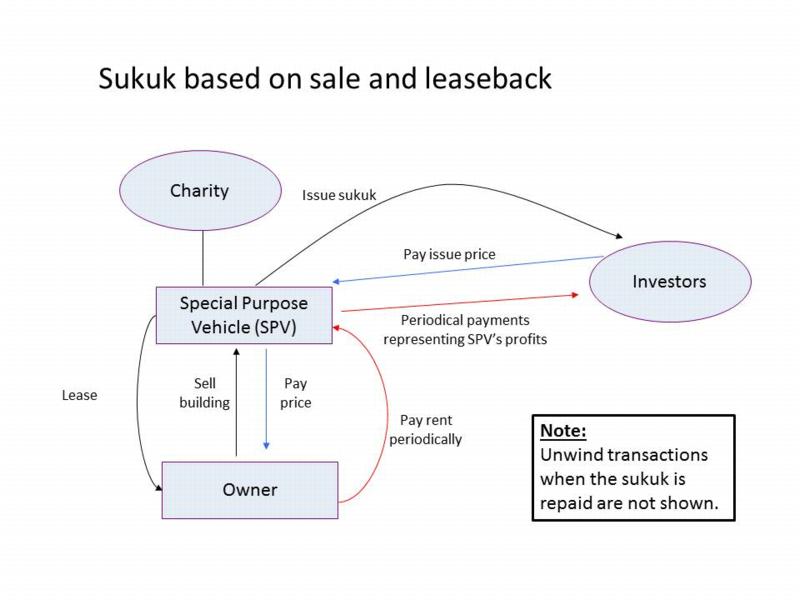

The manner in which these goals are achieved is most easily considered by looking at an example of a sukuk based upon a leasing contract. The owner of a building wishes to use that building to raise finance. Accordingly, the following transactions take place:

These transactions are illustrated in the diagram below.

Although the above sukuk has been designed to replicate the economics of a 5 year bond paying interest of 5% per year, the transactions do not involve the creation of any debts, and no interest is paid. Instead the investors receive rent on the building for 5 years.

The greatest risk to investors in the sukuk is that the obligor/owner fails to pay the rent, or fails to repurchase the building when it is due to do so on the date specified in the sukuk agreements. If those failures occur, the investors are exposed to not receiving what they expected when they bought the sukuk.

Sovereign entities normally pay their obligations in full. This is especially when those obligations are denominated in a currency which is issued by the sovereign, since if necessary the sovereign can print more money to discharge its obligations.

A sovereign sukuk is a sukuk where the obligor (the Owner in the above diagram) is a sovereign entity, typically a state such as the United Kingdom if it proceeds to issue a sukuk.

Such sukuk are regarded as very low risk investments.

There are structures other than sale and leaseback which can be used to issue sukuk. Sukuk can also be designed which are convertible into shares, or which have partial or complete equity characteristics, or which are perpetual.

Such complications are not illustrated as this page was written to provide a simple introduction.

Follow @Mohammed_Amin