Serious writing for

serious readers

Summary

22 October 2011

I gave a presentation on 20 October 2011 at the Middle East and North Africa (MENA) Tax Forum in Istanbul organised by the International Tax Information Center.

The audience mainly comprised delegates from tax authorities in the MENA region, and the conference was strongly supported by the Turkish Ministry of Finance with the keynote address being given by the Finance Minister Mr Mehmet Simsek.

My goal was to illustrate why Islamic finance transactions often cause difficulties for tax systems, as an aid to considering what tax changes might be appropriate to enable Islamic finance to operate without suffering excessive taxation costs. The linked slides contain my presentation with just a few notes added to make it easier to follow without me speaking to the slides.

I have also set out below some additional notes on the kinds of issues that arise, focusing primarily on cross-border issues.

This list is based upon Islamic finance transactions commonly seen in the UK.

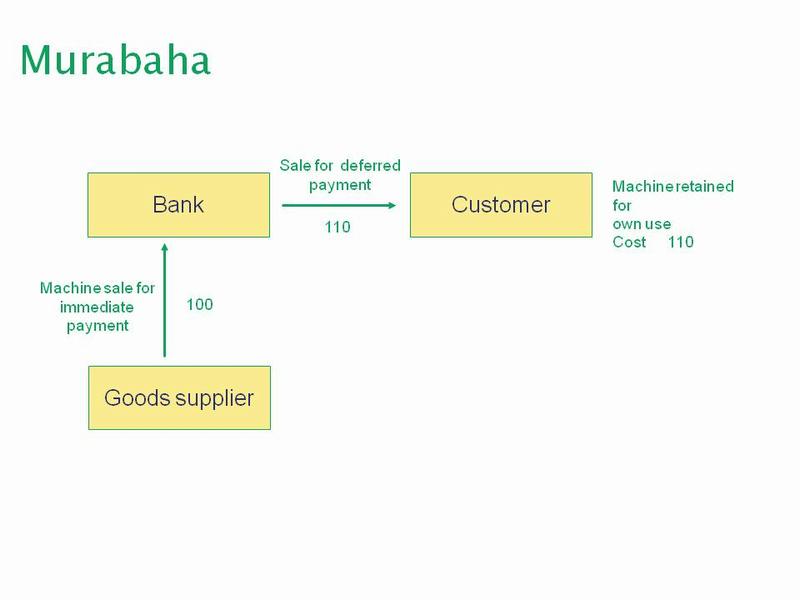

Diagram of a murabaha transaction

The above diagram illustrates a straightforward murabaha transaction. The customer wishes to have use of a machine but cannot afford the purchase price. Instead, a bank will buy that machine for, say, $100 and sell it to the customer for a price of $110, payable at a fixed future time. The customer obtains immediate use of a machine worth $100, and has an obligation to pay $110 in, say, two years time. The extra $10 that the customer pays is clearly, in economic terms, the cost of the finance. However, the legal form of the transaction is that the customer is paying $110 to the bank to purchase the machine.

From a taxation perspective, there are two alternative ways that the customer could be treated.

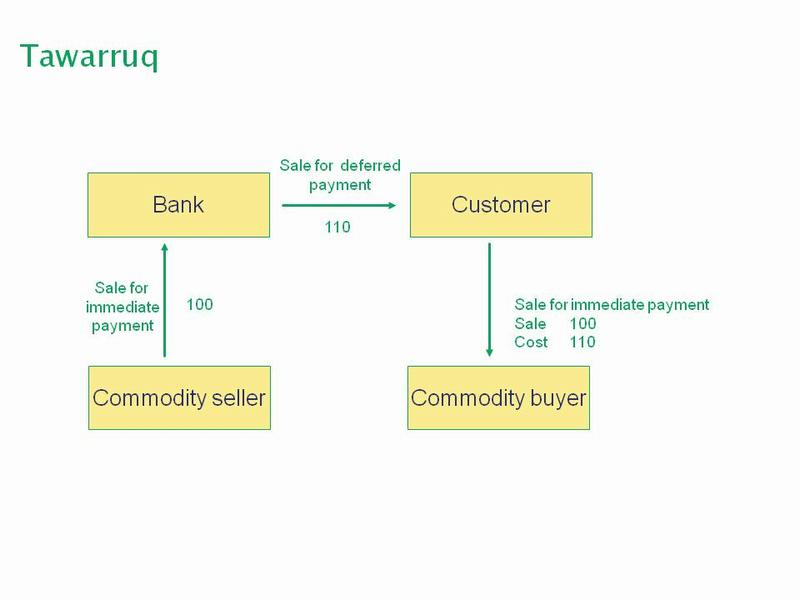

Diagram of a tawarruq or commodity murabaha transaction

In this case, the customer has a desire for cash which the bank wishes to provide without creating an interest bearing loan.

The bank will buy something that can be sold very easily afterwards, with little difference between the bid/offer (buy/sell) prices. A typical example would be a quantity of copper bought on a commodity market. The bank buys the copper, immediately paying $100 for it, and transfers ownership to the customer at a price of $110 payable in, say, two years’ time.

The customer can then immediately sell the copper for a price of about $100. This gives him cash equal to what the bank has laid out, $100, and an obligation to pay the bank $110 in two years’ time. The extra $10 is in economic terms the cost of the finance.

The issue to be decided is whether the customer is entitled to a tax deduction. The customer has purchased an amount of copper at a price of $110 payable in two years’ time, and sold that copper for $100 with the price being payable immediately.

If the tax system of the country concerned decomposes the transaction into its economic substance, then it is clear that the customer has obtained the immediate use of $100 in exchange for the obligation to pay $110 in two years’ time. That extra $10 would then be treated as a finance cost and tax deductible if an equivalent payment of interest would have been tax deductible. (Many countries have limitations on the circumstances in which interest expenses are tax deductible, which are beyond the scope of the discussion on this website page. Instead, the goal is to examine whether a cost of Islamic finance obtains equivalent tax treatment to conventional finance used in the same circumstances.)

However, the tax systems of some countries will not decompose the transaction as analysed above. The legal form is that the customer has actually purchased an amount of copper at a price of $110 and then sold that copper, for immediate payment, at a price of $100. Accordingly, its loss has arisen on the purchase and resale of copper.

Such a loss on the purchase and resale of a commodity may not be tax deductible. In the UK, for example, unless the customer can show that it is trading (as understood by tax law) in copper, it will not be entitled to deduct the $10 loss against its other income. Furthermore, even if the customer regularly trades in copper, this transaction does not look like a legitimate trading transaction since the customer knew that it would suffer a $10 loss when it commenced the transaction. (Trading is normally done with a view to profit.) Accordingly, under UK tax law (before specific changes to facilitate Islamic finance), the customer would not be expected to obtain tax relief for its $10 cost.

Islamic banks typically offer two distinct forms of accounts: current accounts, which are repayable in full but which give the investor no economic return, and savings accounts, which at least conceptually are exposed to the risk of loss but where the customer participates in the profits made by the bank from the use of the customer's money.

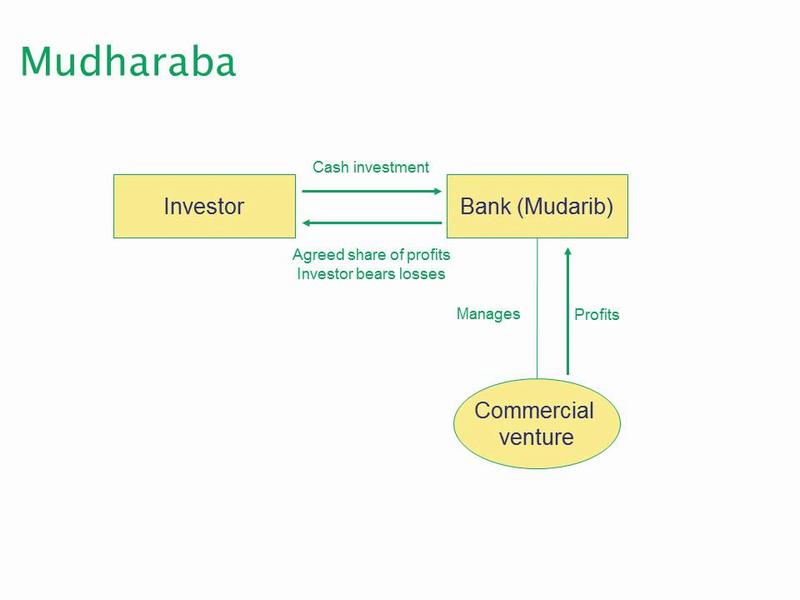

One such form of savings account is a mudharaba based profit and loss sharing investment account (PSIA). This is illustrated in the following diagram.

Diagram of a mudharaba transaction

In a mudharaba transaction, the investor (the depositor in the bank) provides cash to the bank (acting as mudarib) to invest that money in a commercial venture, with the bank as mudarib managing that commercial venture. Typically, in the case of a bank the commercial venture will consist of the full range of its operating assets, both loans (transacted in Islamic form) to customers and financial assets held in the bank's treasury operations to ensure that the bank has sufficiently liquidity to repay its current account and savings accounts customers when required.

If there are profits from the bank’s operations, those profits are shared between the bank and the customer on an agreed basis. Typically, the customer obtains a return similar to market interest rates while the bank keeps any excess return as a reward for organising the transactions.

Most tax systems would be expected to tax the investor on the profits paid to it. Similarly, one would expect the bank to be taxed on all the profits that it makes from its operations while receiving a deduction for the profit sharing payments that it makes to its customers.

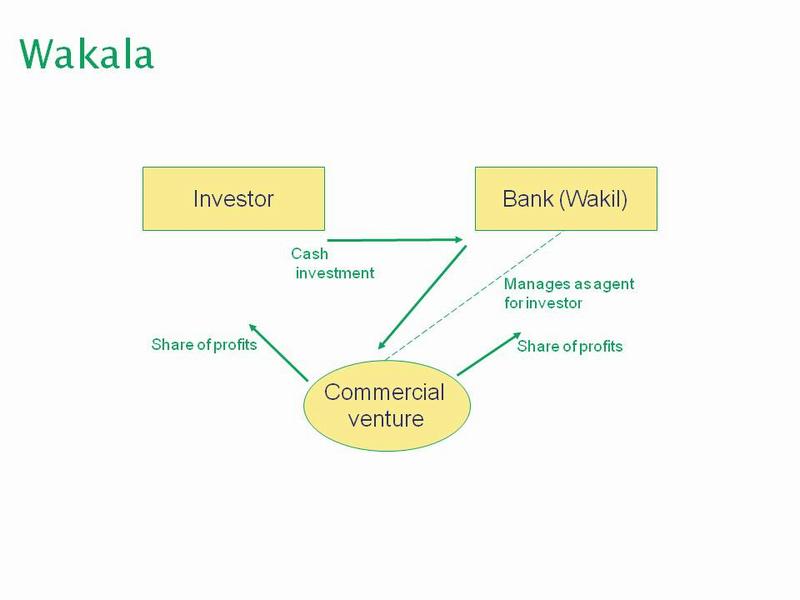

Another form of contract which can be used for an investor to provide money to a bank to earn an economic return is a wakala contract.

Diagram of a wakala transaction

In wakala, as with mudharaba, cash is going from the customer as an investor and is used to finance a commercial venture with the profits of the commercial venture being shared between the investor and the bank (the wakil) in agreed proportions.

This is often used for people buying houses for owner occupation instead of a conventional mortgage, but can also be used for the purchase of investment property. It is illustrated in the following diagram.

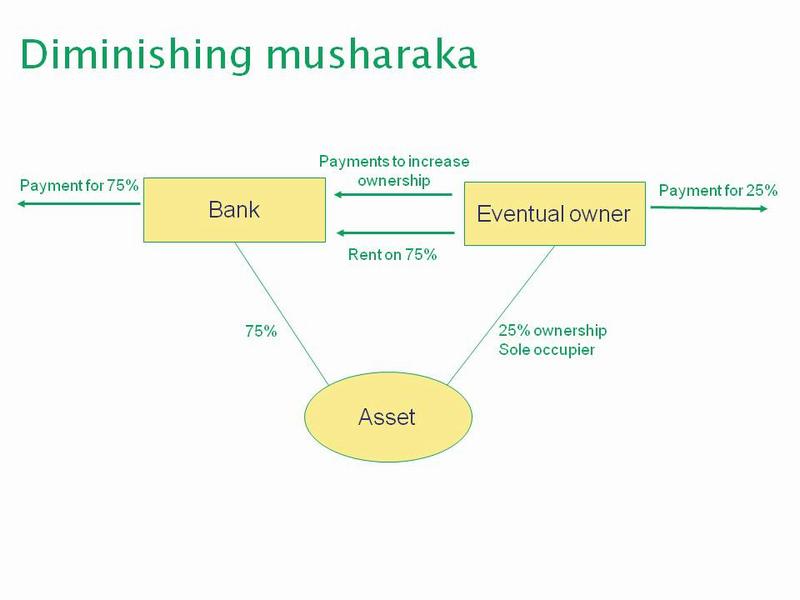

Diagram of a diminshing musharaka transaction

Diminishing musharaka is used when one party, here called the eventual owner, wants to buy an asset but cannot afford to pay for all of it. In the diagram, on day one the bank buys 75% of the asset, for example a building, while the eventual owner buys 25%. Under the contract between the eventual owner and the bank, the eventual owner has immediate rights to sole occupation.

The eventual owner pays rent to the bank on the 75% of the property that it doesn’t own. Then, over the life of the arrangement, as well as paying the rent, the eventual owner will make additional payments to the bank to purchase additional slices of the asset.

The price for the additional slices of the asset will be set out in the diminishing musharaka agreement. While any price formula can be used, in practice two arrangements are most common:

At first sight, one would expect the eventual owner to receive tax relief for the rent that it is paying to the bank. This rent is being paid to enable the eventual owner to occupy the whole of the building even though it only owns 25% initially.

However, upon a closer analysis, tax relief for the whole rent is not entirely certain. This is because the eventual owner also has the right to purchase the bank’s share of the property over an extended time period.

If the purchase of additional slices will be at market value, then the rent that the eventual owner is paying does no more than entitle it to occupy the property. The level of the rent is likely to be the same as the rent that is paid in conventional property rental transactions where there is no intention for the tenant to purchase the property. Accordingly, in this scenario the entire rent should be tax deductible.

The analysis is different if the eventual owner is entitled to purchase of the bank’s share of the property at a price equal to the original price paid by the bank. In this situation, the rent paid by the eventual owner actually achieves two things:

This preservation of the entitlement to purchase at original cost has the nature of the payment for an option to the purchase of the building, rather than being a payment for the right to occupy the building. This can be demonstrated by considering the amount of the rent: one would expect this to be higher than the level that would be paid by a conventional tenant merely for the occupation of the property, as the eventual owner has greater rights than would a conventional tenant. Logically this additional element of the rent should be denied tax relief as being linked with the entitlement to purchase the property at the bank's original cost.

The goal when structuring a sukuk is to replicate the characteristics of bonds without infringing the rules of Shariah. The most important requirement is that there must be no interest, which in turn means that there can be no legal debt involved.

The goal is to design an instrument which:

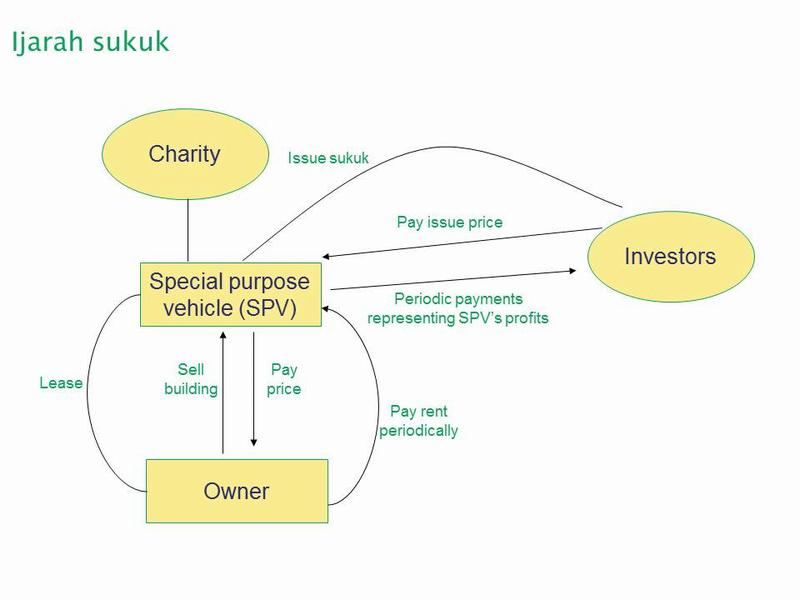

The diagram below illustrates how an ijarah sukuk transaction where real estate is the underlying asset would normally be arranged.

Diagram of an ijarah sukuk transaction

The owner of a building wishes to use that building to raise finance. Accordingly, the owning company arranges for the creation of another company, typically a special purpose vehicle (SPV). This is a company which is not part of the owner company’s group; the shares of the SPV are normally held by a charity. The SPV raises the cash needed to purchase the building by issuing sukuk to the investors.

Legally, the sukuk are certificates which entitle the investors to a fractional share of the building. The SPV will normally declare itself as a trustee of the building on behalf of the sukuk investors, so that they have a beneficial entitlement to a proportionate share of the building and of the rent receivable from leasing it.

During the life of the sukuk, the owner will pay rent to the SPV which in turn will pay that money on to the investors. In economic terms, the investors have a prior claim on the profits generated by the owner from its business because part of those profits must be used to pay rent on the building to the SPV prior to any distribution of profits to the equity shareholders. However, this is achieved without creating a debt since leasing a building does not involve a debt claim.

At the end of the sukuk period, the owner will purchase the building back from the SPV and this provides the SPV with cash to repay the sukuk investors.

This transaction raises several potential taxation questions. Firstly, there are three land transactions, namely the original sale of the building to the SPV, the lease of the building by the SPV back to the original owner and finally the re-acquisition of the building by the owner. Each of these is potentially subject to real estate transfer tax or similar taxes on the leasing of land. Furthermore, the building may have appreciated in value between the original purchase by the owner and its sale to the SPV. Accordingly, the sale transaction may trigger a taxable capital gain.

When one considers the SPV, it is receiving rental income on the building which would normally be taxable. It then passes on that rental income to the sukuk holders who are therefore suffering taxation prior to receiving their cash. Conversely, if they had invested in conventional interest-bearing bonds, such bonds normally pay their interest gross without withholding tax.

The following is a short list of some taxation issues that often arise.

Islamic finance transactions often involve multiple transfers of an asset (often real estate) where the equivalent conventional transaction does not require asset transfers. Accordingly Islamic finance transactions may suffer multiple instances of transfer taxes, especially if the country concerned operates a real estate transfer tax.

Where an asset is sold by the owner in order to raise finance, with the asset subsequently being re-acquired, that may be treated as a disposal for capital gains tax purposes. Accordingly capital gains tax may be payable with Islamic finance transactions even when there is no change in the party that has the economic benefits and risks of ownership.

It is generally accepted by most countries that where a foreign bank makes an interest-bearing loan to a borrower located in a second country, then unless it has a branch located in that second country which is effectively connected with the making of the loan, the bank is not liable to business profits taxes in that second country. (Of course withholding taxes discussed below may be payable on interest paid from the second country to the bank.)

However an Islamic finance transaction such as a commodity murabaha transaction may involve the foreign bank (either directly or through agents) purchasing and selling assets located in a second country. It is possible that such activities could cause the foreign bank to be treated as having a permanent establishment in that second country.

The same issues apply if money is provided to a bank using mudharaba or wakala. The role of the bank in acting as agent or partner for the customer may have significant consequences in international transactions. The bank acting as agent or partner for the customer in providing funds to the underlying commercial venture may be sufficient to cause the customer to have a permanent establishment within that country since the bank as agent is taking commercial decisions on the customer's behalf.

The consequence may be to make the customer taxable on the profit paid to it whereas interest paid on a conventional bank deposit to a foreign person may not have been taxed by that country, either due to the country's domestic tax law or because many double taxation treaties give exclusive taxing rights on interest to the country where the customer is resident rather than to the country of source. Accordingly, replacing a conventional deposit with a wakala contract or a mudharaba contract involves the risk of creating a taxable presence in the country where the bank is located.

Many countries have withholding taxes that are charged on payments to foreign persons. It is common to have a withholding tax on interest paid to foreigners, with the rate of withholding tax being reduced (often to zero) where a double taxation treaty applies.

The cross-border payments made with Islamic finance transactions are legally different from those made in conventional transactions. For example none of them is legally a payment of interest. Accordingly the question arises as to how withholding taxes should be charged on Islamic finance transactions and at what rates.

As an illustration, if a foreign bank makes an interest-bearing mortgage loan to a borrower in a second country, that second country may apply withholding tax on the interest payments that the borrower makes to the bank. However if the finance is structured as a diminishing musharaka transaction, the payment by the householder to the bank will be rent in respect of the occupation of the property. The second country may apply a different rate of withholding to rent paid to foreign persons than it applies to interest paid to foreign persons.

Almost all existing double taxation treaties were negotiated in an environment where almost all financial transactions comprised conventional finance. Accordingly they are unlikely to make specific provision for Islamic finance transactions and in many cases may not be readily adaptable to Islamic finance.

For example many double taxation treaties reduce the rate of withholding tax on cross-border payments of interest. However the definition of interest under the treaty may not be extensible to payments which are economically equivalent to interest made under Islamic finance transactions. Accordingly if the country from which the payment is being made charges a withholding tax on the payment, the recipient may not qualify for reduced withholding even if there is a double taxation treaty which would reduce the rate of withholding tax on an equivalent interest payment.

For example, Article 11(3) of the OECD model convention 2010 defines interest as follows:

3. The term “interest” as used in this Article means income from debt-claims of every kind, whether or not secured by mortgage and whether or not carrying a right to participate in the debtor’s profits, and in particular, income from government securities and income from bonds or debentures, including premiums and prizes attaching to such securities, bonds or debentures. Penalty charges for late payment shall not be regarded as interest for the purpose of this Article.

This definition does not accommodate payments made under Islamic finance transactions which are economically equivalent to interest, since such payments do not arise from a debt-claim.

In a few cases, countries negotiating double taxation treaties have included a wider definition of interest. For example, the definition of interest in Article 11(2) of the current UK/USA double tax treaty reads as follows:

The term "interest" as used in this Article means income from debt-claims of every kind, whether or not secured by mortgage, and whether or not carrying a right to participate in the debtor's profits, and, in particular, income from government securities and income from bonds or debentures, including premiums or prizes attaching to such securities, bonds or debentures, and all other income that is subjected to the same taxation treatment as income from money lent by the taxation law of the Contracting State in which the income arises. Income dealt with in Article 10 (Dividends) of this Convention and penalty charges for late payment shall not be regarded as interest for the purposes of this Article.

The United Kingdom has brought in legislation which for taxation purposes treats income arising from defined transactions (transactions which are commonly carried out in Islamic finance) in the same manner that interest is treated for taxation purposes. The underlined words in the above definition have the effect of applying the treaty to such payments in exactly the same way that the treaty applies to interest.

Under the VAT rules applicable within the European Union, financial transactions are normally treated as "exempt" from VAT. The consequence is that banks do not charge VAT when charging interest to customers but conversely because most of a bank’s transactions are exempt, the bank is able to recover very little of the VAT that it suffers on its costs.

Islamic finance is normally provided by carrying out transactions that involve real assets. In many cases the supply of those assets will be subject to VAT. (Not always; for example the commodity that is the subject of a commodity murabaha transaction may be located in a third country or inside a bonded warehouse with no VAT arising on its sale provided the commodity's location does not change.) If VAT is charged on the supplies of assets involved, this may give rise to additional costs if the party to the Islamic finance transactions is not able to recover the VAT.

Conversely, if the parties to the transactions are able to recover the VAT then there may be an overall loss of tax revenue since the bank which facilitates the transactions may now be able to recover VAT on a higher proportion of its costs since it is making increased taxable supplies while there is no increase in the net VAT payable by the parties to the transactions since they are recovering any VAT suffered.

Follow @Mohammed_Amin