Serious writing for

serious readers

If external Shariah audit is introduced, there is no need for a Shariah Supervisory Board to confirm Shariah compliance to shareholders. Its retention would risk causing confusion about where responsibility for Shariah assurance lies.

Summary

26 December 2016

On 26 October 2016, I attended a very interesting conference on "Shariah Governance" organised jointly by the International Shari’ah Research Academy for Islamic Finance (ISRA) and the Islamic Finance Council UK (UKIFC).

Apart from the presentations and related discussion, the event saw the UK launch of the two organisations' joint document "External Shari’ah Audit Report" which had been published earlier in the month.

While introducing external Shariah audit (ESA) has much to commend it, in my opinion the published document fails to address the implications for the Shariah Supervisory Board (SSB). I explain below why I believe any introduction of ESA should be accompanied by the abolition of the SSB.

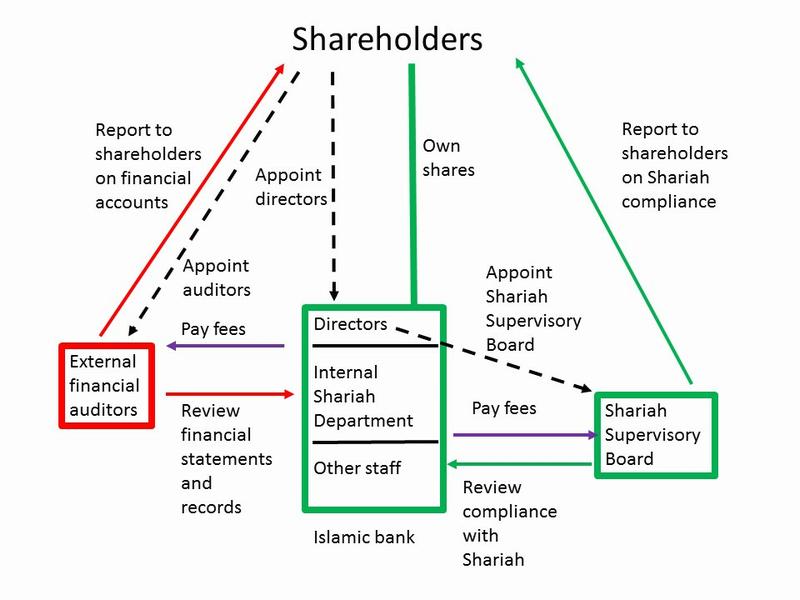

The diagram below sets out the current financial and Shariah governance structure of Islamic banks, and is equally applicable to takaful companies.

The shareholders appoint the directors of the Islamic bank and have the power to remove them. The shareholders also determine the pay of the directors.

The directors have the responsibility for running the Islamic bank. While they appoint the directors, the shareholders have no role in managing the Islamic bank.

In turn, the directors are responsible for hiring and supervising both the general banking staff, and the internal Shariah department (ISD). While the ISD consists of employees having specialist Shariah knowledge, they report to the directors in the same way as employees with specialist legal knowledge or specialist accounting knowledge.

None of the employees of the bank are independent, since they are hired and fired by the directors.

The firm to be appointed as external financial auditors (EFA) is normally initially selected by the directors.

It is now standard practice in countries such as the UK and many other jurisdictions for the initial selection to be made by the Islamic bank's audit committee. Furthermore, the audit committee is now normally comprised entirely of independent director who do not work day to day at the bank, unlike the management directors.

However the EFA are then formally appointed by the shareholders. The directors do not have the power to remove the EFA. The shareholders normally delegate to the directors the task of agreeing the EFA's fees.

The EFA carries out what work the EFA considers necessary, and then issues a formal report to the shareholders on whether the Islamic bank's financial accounts comply with the applicable accounting standards and with any legal requirements of the jurisdiction of incorporation.

It is virtually universal practice for Islamic financial institutions to have a Shariah Supervisory Board (SSB).

The ISRA/UKIFC document on page 13 states that the guidelines of the Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI) are for the SSB to be appointed by the shareholders, as quoted below. (Emphasis added):

AAOIFI has adopted a four-tier approach towards Shari’ah governance: external audit of financial statements, SSB, audit and governance committee (AGC), and internal Shari’ah review.

External auditors of financial statements and members of the SSB are appointed (and also dismissed) by the shareholders in the AGM upon recommendation of the board of directors (BOD), taking into consideration local legislation and regulations. Their separate reports are published as part of the annual report of the IFI.

That is confirmed by looking at AAOIFI's Governance Standard 1 "Shari'a Supervisory Board: Appointment, Composition and Report" which specifies in paragraph 3:

Every Islamic financial institution shall have a Shari’a supervisory Board to be appointed by the shareholders in their annual general meeting upon the recommendation of the board of directors taking into consideration the local legislation and regulations. Shareholders may authorise the board of directors to fix the remuneration of the Shari’a supervisory board.

However this standard is not followed universally. In Malaysia the Central Bank has published its guidelines on the goverance of the Shariah committee. Paragraph 8 specifies:

8. The Board of Directors of an Islamic financial institution upon recommendation of its Nomination Committee shall appoint the members of the Shariah Committee. The appointment and reappointment of a Shariah Committee member shall obtain prior written approval of Bank Negara Malaysia. The appointment shall be valid for a renewable term of two years.

Accordingly the shareholders do not appoint the SSB. However there is external vetting since the Central Bank has to approve the appointment.

In the UK, the Government does not regard itself as a religious regulator, and there are no specified rules regarding how the SSB is appointed. The International Monetary Fund working paper WP/14/220 "Islamic Banking Regulation and Supervision: Survey Results and Challenges" by Inwon Song and Carel Oosthuizen contains some findings on pages 16 - 18. The short extract below shows that there is no uniformity in practice, despite the standard specified by AAOIFI:

Legal frameworks require the setting up of a Shariah board for an Islamic bank in 17 jurisdictions surveyed. In addition, on the status of the Islamic bank’s Shariah board, five respondents indicated that it was a subsidiary organ of the general assembly of shareholders; eight respondents indicated it was a free-standing organ; two respondents mentioned it was a subsidiary organ of the board of directors.

There appears to be heterogeneity regarding the bodies to which the Shariah board reports to. These may include: the board of directors of the bank (eight respondents), the general assembly of the bank (eight respondents), the top management of the Islamic bank (two respondents), the executive committee of the Islamic bank (two respondents), and the bank (one respondent).

The finding in the IMF Working Paper is consistent with my own very small scale survey. In the UK, the website of Gatehouse Bank plc states: "The SSB is formally appointed by the Board of Directors, pursuant to the delegated authority of, and reporting directly to, the Bank’s shareholders." In Qatar, the 2015 accounts of Qatar Islamic Bank were silent on how the SSB is appointed.

Accordingly, my educated guess is that in most cases the SSB is appointed by the Board of Directors, and I have shown it as such in the diagram above.

All of the Islamic bank accounts I recall reading over many years have contained a report from the SSB on compliance with Shariah which is addressed to the shareholders, except where the SSB report does not specify the addressee, as with Qatar Islamic Bank 2015 on page 44.

The key issue is that during the year the SSB gives advice to the Islamic bank on prospective transactions. Accordingly, at the end of the year, it is at risk of reviewing its own work.

The ISRA/UKIFC publication expresses this concern on page 9:

In parallel to the conventional external auditor, it has been a common practice for the SSB of an IFI to issue an annual opinion certifying that the contracts, transactions and dealings of the IFI are in compliance with Shari’ah. In arriving at this conclusion, the SSB undertakes an audit but mostly relies on the work of the internal Shari’ah compliance unit/review department.

At present, there is no independent third party publicly reaffirming the view of the SSB on Shari’ah compliance. This immediately raises a number of questions, most fundamentally: Are the SSB members inadvertently in danger of being in an impaired position in that they are being asked to audit products they themselves have designed and signed off as compliant? Is there a need for an additional independent external check on Shari’ah compliance; and if so, then what should be its scope?

The ISRA/UKIFC publication looks at the practice of Oman and Pakistan where the regulators are implementing ESA and also includes views from Bahrain and Malaysia.

However the final part of the publication, despite being called "Conclusion" is actually inconclusive! It points out various difficulties with what is happening at present, but does not make clear, specific recommendations, which is what one expects in a "Conclusion" section.

In my view there are two alternative ways forward.

If one is happy with the structural independence of the SSB, but has concerns about its ability to audit large numbers of transactions, that work can be delegated to the EFA.

I explained this in more detail in my November column in "Islamic Finance News" with the title "Who should do what in Shariah governance?" which is reproduced below.

If the SSB is not considered sufficiently independent, then an ESA can be engaged. (That could consist of appropriately qualified people within the EFA, or an entirely separate organisation.)

The key point here is that there should not be two separate reports to the shareholders on Shariah compliance. If ESA is to be introduced, there is no longer any scope for a report from the SSB, and actually no need for an SSB at all.

I explained this in more detail in my December column in "Islamic Finance News" with the title "Retaining an independent Shariah Supervisory Board is incompatible with External Shariah Audit" which is also reproduced below.

I believe greater clarity is needed regarding the Shariah governance of Islamic financial institutions (IFIs)

Ultimately, the Board of Directors (BoD) are responsible for managing the IFI and ensuring that it has proper Shariah governance in place. Standard industry practice is for the BoD to appoint an external Shariah Supervisory Board (SSB). The SSB members are not employees of the IFI but external contractors who can demonstrate expertise on matters of Shariah. They are not subject to the orders of the BoD.

It should be the responsibility of the SSB to set out clear written policies regarding what transactions the IFI may engage in without ceasing to be Shariah compliant, and if necessary detailed rules on how those transactions should be structured. If the IFI engages in bespoke transactions, each such bespoke transaction should be reviewed by the SSB in advance to decide whether the transaction will be Shariah compliant. While it is not industry practice to publish the full text of all SSB fatwas (detailed Shariah analyses leading to an opinion) I believe it should be.

Unlike the SSB, the IFI’s internal Shariah department (ISD) is a team of employees answerable to the Board of Directors. The ISD can answer questions raised by other employees if the answer is clearly determinable from either external published guidance (such as the AAOIFI Shariah Standards) which has been approved in advance by the SSB or from the SSB’s own written policies. In my view the ISD should consult the SSB before taking a position on any other Shariah questions.

Everything so far discussed is prospective. Once the financial year has been completed, the IFI needs to determine whether it has conducted its affairs in a Shariah compliant manner, just as it needs to determine whether its accounts give a true and fair view in accordance with applicable accounting standards.

The IFI’s external auditors will of course provide their opinion on whether the financial accounts give a true and fair view. The key question is who should give an opinion on whether the IFI has conducted its affairs in a Shariah compliant manner. Current practice is for this opinion to be given by the members of the SSB. However, to do so they need to enquire into the actual conduct of its affairs by the IFI throughout the year.

Where the IFI undertakes many transactions, the SSB members will not have the manpower, and may lack the skills, to audit large numbers of transactions for Shariah compliance. They risk relying upon an internal Shariah audit report from the ISD which however is not independent. Where the IFI has conducted only a few bespoke transactions, the SSB is likely to have been involved in some detail in their implementation. It is then at risk of auditing its own work.

In my view, all auditing of completed transactions should be carried out by the external auditors. Their purpose should be to ensure that the transactions are compliant with the SSB’s advance requirements. The auditors would not report that “we consider that the IFI has been Shariah compliant” but rather “we consider the transactions carried out by the IFI compliant with the SSB’s requirements.” In turn, the SSB could then give its opinion that the IFI has been Shariah compliant.

I do not see any role for a second external party to give an opinion on whether the SSB’s opinion is correct, just as no company has a second external auditor “second guessing” whether the external auditors opinion is correct.

Shariah governance is currently much discussed. Many propose adding the function of external Shariah audit (ESA) to mirror the role of external financial audit. However, in my view insufficient thought is being given to the implications of ESA for the role of the Shariah Supervisory Board (SSB).

All financial institutions must obviously comply with state law and with accounting standards, normally IFRS. In addition, Islamic financial institutions must also comply with the rules of Shariah as specified by:

Compliance with standards, whether accounting or Shariah, is rarely a black or white issue but is normally a matter of finely judged opinion. For accounting, the opinion which matters is that of the external financial auditor (subject to the oversight by the courts in the event of negligence, unlawful behaviour etc.) The BoD is responsible for preparing the accounts, but will be aware that if the external financial auditor disagrees with the financial institution’s accounting and qualifies his opinion, shareholders and the market generally are overwhelmingly likely to follow the view of the external financial auditor since he is recognised as an expert and as being independent.

The above model maps perfectly well to compliance with Shariah standards. The BoD is responsible for managing the Islamic financial institution and ensuring that it complies with Shariah. At the end of the financial year, the ESA can audit what has happened and give his opinion regarding whether what has been done complies with Shariah. Obviously, during the year, the BoD is free to consult Shariah experts if it wishes (as it similarly consults legal experts and accounting experts) but it is the BoD which takes responsibility for the actions of the Islamic financial institution and the transactions undertaken.

The problem with the above model is squaring it with the present role of the SSB.

At present, the SSB is held out as being independent of management, and the members of the SSB are named in the annual report and they give an opinion regarding whether the Islamic financial institution has complied with Shariah. This risks confusion if the independent SSB gives one opinion while the independent ESA gives the opposite opinion.

If an opinion regarding compliance with Shariah is to be given by an independent ESA, then in my view there is no role for an independent SSB. Obviously, the Islamic financial institution will employ staff expert on Shariah in the internal Shariah department. If during the year the BoD considers that additional Shariah expertise is required for specific purposes (just as external lawyers are often hired for complex projects even though the institution has an internal legal department) then of course they are free to purchase such additional Shariah expertise from external consultants. However, there should be no special status for such external Shariah consultants. The SSB as presently constituted should be entirely abolished if an ESA is appointed. Otherwise the SSB’s continued existence would cause confusion with the role of the ESA.

Follow @Mohammed_Amin