Serious writing for

serious readers

Summary

Posted 20 March 2015

The magazine "Journal of International Taxation" is published by Thomson Reuters. Through my fellow author Hafiz Choudhury I was asked by a member of the editorial team, Robert Gallagher, to write an article based upon the report "Cross border taxation of Islamic finance in the MENA region Phase One".

In writing the article, the intended reader I had in mind was the tax director of a multinational corporation who is not a specialist in Islamic finance.

I understand it was published in the January 2015 issue. What I have reproduced below is the article I submitted, which had to be abridged slightly due to the magazine's space constraints.

Islamic finance presents a challenge for tax systems that have generally been developed within a framework of conventional financial transactions.

Mohammed Amin MA, FCA, AMCT, CTA (Fellow) is an Islamic finance consultant and previously UK Head of Islamic Finance at PricewaterhouseCoopers LLP. The Journal thanks Hafiz Choudhury, a Principal with The M-Group in Washington, D.C., for his help in coordinating publication of this article.

During 2012 the author was the lead researcher for a project looking at the cross-border taxation of Islamic finance in the Middle East and North Africa region (MENA). This was a joint project of the International Tax and Investment Centre (Washington DC) and the Qatar Financial Centre Authority (Doha). It resulted in an 84 page report "Cross border taxation of Islamic finance in the MENA region Phase One" which can be downloaded free from the QFCA website.

This article has the following objectives:

The Islamic finance industry has grown steadily for several decades from a very small base, beginning with a couple of small banks in the 1960’s. Globally Islamic financial assets are now in the region of $2 trillion. While this still represents less than 1% of global financial assets, that percentage is expected to continue increasing as Muslims constitute about 23% of world population and many Muslim majority countries are experiencing significant economic growth. The result is that Islamic finance is moving beyond being an exotic niche of interest only to specialists.

Accordingly MNCs which sell financial services should consider whether they can afford to ignore a market with such a strong long-term growth trend. Furthermore tapping Islamic finance offers the scope to broaden funding sources, and attract new equity investors.

Conventional financial services are normally divided into the following categories:

From a religious perspective each of the above can present difficulties to Muslims.

Many Muslims believe that the receipt or payment of interest is prohibited. Religious scholars also express concerns about other factors such as excessive uncertainty in contracts. Furthermore many Muslims believe that if an activity is prohibited to Muslims (such as the consumption of alcohol) they should not engage in promoting that activity (for example by owning shares in a brewery company).

Accordingly, there are distinct approaches used by Islamic finance in each of the above areas. This article and the research it is based upon address only banking and debt capital markets.

Working together financiers and the religious scholars have devised transactions which achieve the same economic effect as conventional financial transactions without violating Islamic religious principles. These transactions are normally described as being Shariah compliant. (The word "Shariah" is often translated as "Islamic law" but is better understood as a word that encapsulates all of the principles of Islam. It is an Arabic word whose original meaning is the path to water, critical in a desert environment, and which can be understood in religious terms as being the path to salvation.)

The research project specifically considered four structures which are widely used in Islamic finance. In particular it looked at the implications of carrying out these transactions cross-border. Those transactions are set out below as a precursor to discussing the tax issues.

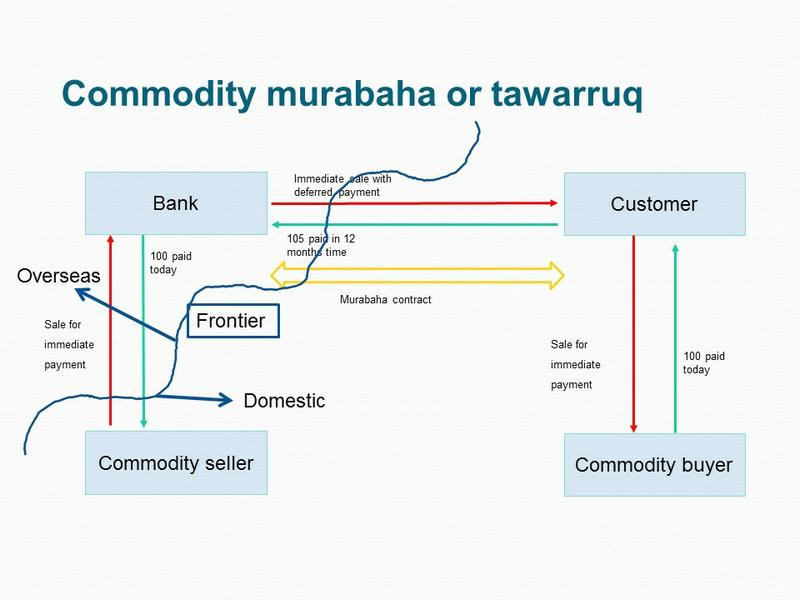

The purpose of this transaction is for a bank to supply an amount of money to its customer, and for the customer to be liable to pay a fixed larger amount of money back to the bank on a fixed future date. This is to be accomplished without having an interest bearing loan which would be prohibited under the rules of Islamic finance.

Accordingly, the bank sells its customer a commodity on deferred payment terms, with the customer selling the commodity to obtain cash. This is illustrated by the diagram below.

The bank is located overseas and the commodity is copper. The bank purchases copper from a commodity seller for immediate delivery and payment. The bank then sells the copper to the customer for a higher price which is deferred, but delivers the copper immediately. The customer then sells the copper for cash.

In cash terms, Customer receives cash of $100 now, and pays cash of $105 to Bank in 12 months’ time.

“Murabaha” is the Arabic name for a transaction which involves one party purchasing goods and then selling them to a second party at a mark-up to reflect a delay in payment, with the mark-up being fully disclosed to the second party. The name “commodity murabaha” is used as a commodity is used; most commodities are acceptable provided there is a liquid market, but some such as gold or silver are prohibited for religious reasons. The transaction is also known as “tawarruq” because the second party will sell the commodity immediately to obtain cash.

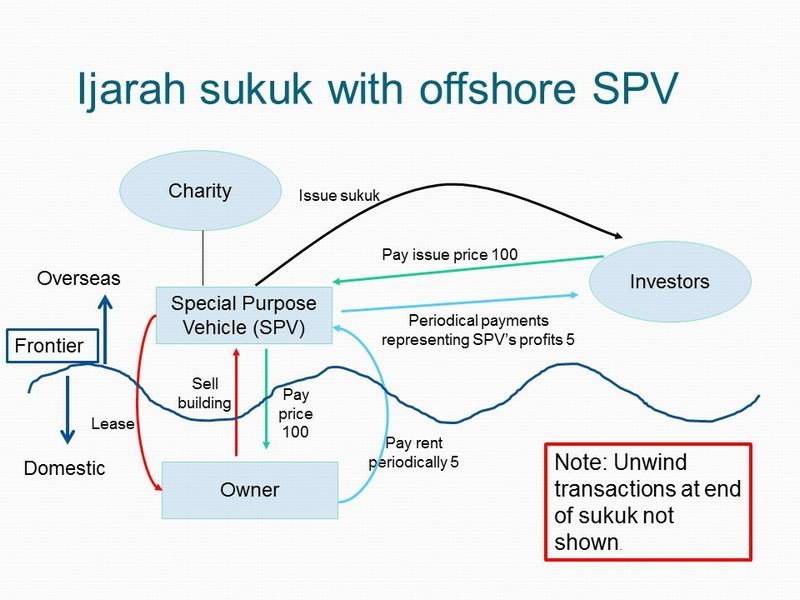

The purpose of the sukuk structure is to create an instrument that can be freely bought and sold between investors. Under the terms of the instrument, the investors in the sukuk will receive a fixed cash payment each year, and they will receive a fixed cash payment when the specified period of the sukuk ends. Accordingly the sukuk have the same economic characteristics as fixed life fixed rate bonds.

These fixed cash payments are achieved by the owner of a building selling the building to a special purpose vehicle (SPV) and then leasing the building paying rent. At the end of the fixed period, the original owner will buy back the building.

Owner owns a building which it purchased many years ago for $20 million. After the SPV has been formed, Owner sells that building to SPV for a price of $100 million. Owner also gives SPV a purchase undertaking by promising that if in five years’ time SPV offers to sell the building to Owner for a price of $110 million, Owner will buy, while SPV gives Owner a sale undertaking by promising that if in five years’ time Owner offers to buy the building from SPV for a price of $110 million, SPV will sell.

Accordingly it is very likely that the building will be sold by the SPV back to the original owner for a price of $110 million in five years’ time.

SPV rents the building to Owner with a lease which is five years long. The rent is $5 million per year, payable once a year with the first payment in 12 months’ time.

SPV creates sukuk certificates under which it holds the building, the lease and the benefit of the Owner’s purchase undertaking as trustee for whoever is the owner of the sukuk certificates. These are sold to investors, located overseas, for a total price of $100 million and the cash is used to pay Owner for the property.

All of the rental payments and the buyback payments take place as planned. Accordingly, at the end of year 5, Owner pays $110 million to SPV and SPV transfers ownership of the building to Owner. SPV passes the $110 million sale price of the building on to the investors in proportion to their ownership of the sukuk certificates and the sukuk certificates are cancelled.

To summarise, for an initial outlay of $100 each investor will receive $5 after 1, 2, 3 and 4 years, and at the end of year 5 will receive $115 (representing $110 for sale back of part of the building and $5 for the final year’s rent.) Accordingly the sukuk instrument replicates the characteristics of a fixed term fixed rate tradable bond.

“Ijarah” is an Arabic word which means leasing. Here the stream of payments received by the investors is achieved by the SPV leasing the building back to the original Owner.

The Arabic word “sak” means certificate (in the sense of certificate of ownership) and “sukuk” is the plural of sak. (In English grammar the word is uniplural.) The sukuk represent fractional entitlements to ownership of the building and to the income generated by the building.

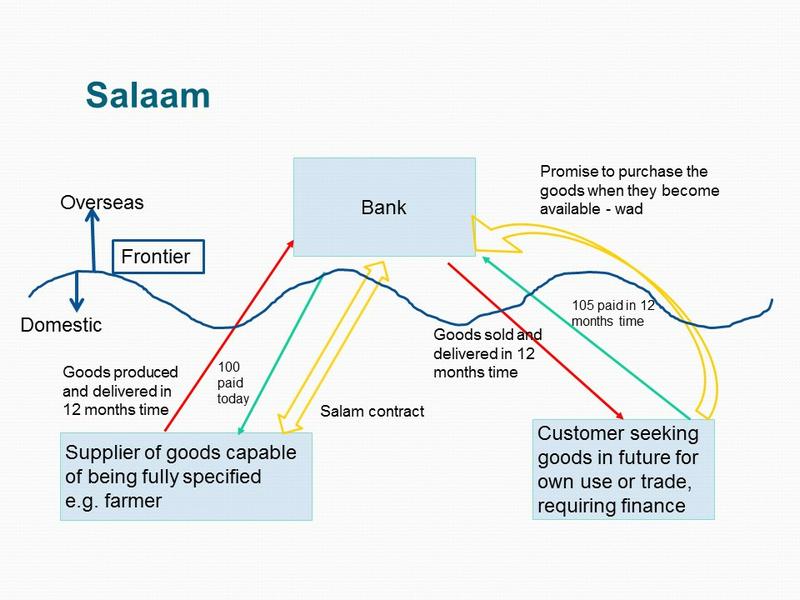

The purpose of the salaam structure is to enable the bank to provide finance to a producer of goods, for example a farmer. The farmer requires cash now, possibly to purchase seeds or fertiliser, while the output will only be produced in the future.

The bank wishes to avoid having an economic exposure to the price of the goods, so it enters into an agreement with a customer who wishes to obtain those goods in the future at a price which is fixed today.

The Bank is located overseas.

A Customer located in the country concerned wishes to receive 300kg of wheat in 12 months’ time, and is willing to commit to paying $105 for that wheat. Accordingly today Customer gives a promise to the overseas Bank that if in 12 months’ time Bank offers to sell 300kg of wheat to Customer for a price of $105, Customer will purchase it.

Supplier is a farmer located in the same country. Today Bank enters into a salaam contract with Supplier under which Bank will pay Supplier $100 immediately and Supplier will agree to deliver 300kg of wheat to Bank in 12 months’ time.

The contracts are completed in due course in accordance with their terms.

“Salaam” in Islamic commercial law is a contract to pay in full now for goods that will be delivered later and which may not yet exist. While Shariah normally prohibits the sale of something that does not yet exist, it makes an exception for certain items such as agricultural commodities that are fungible and are yet to be grown. Most Islamic scholars consider that the salaam contract can only be used for such permissible items.

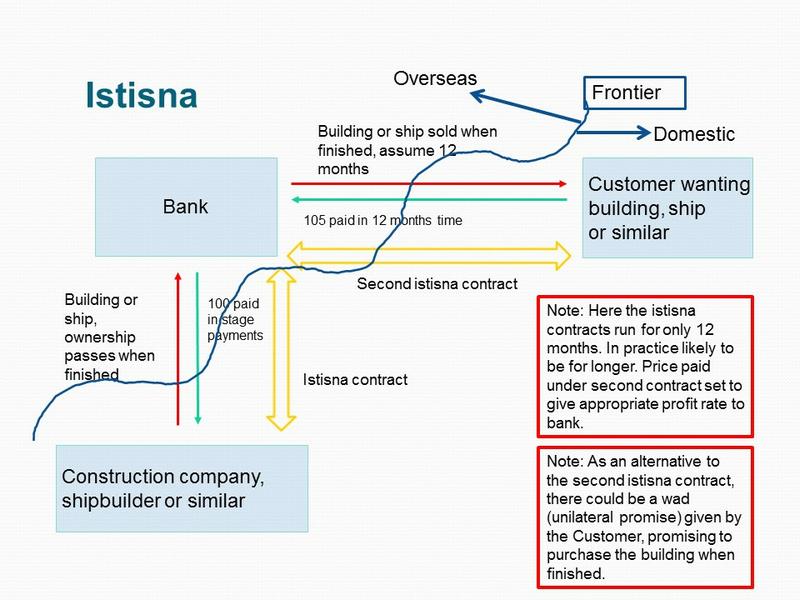

The purpose of the istisna contract is to enable the bank to provide finance which is required by a customer purchasing goods which are to be manufactured to the customer’s specifications. Normally the manufacturer would require the customer to make stage payments, both to reduce the manufacturer’s credit risk against the customer and also to enable the manufacturer to finance the inventory while the goods are being manufactured.

However the customer does not have the funds needed to make stage payments to the manufacturer, and therefore seeks finance from the bank. The bank is willing to take on the customer’s credit risk, but does not want any economic exposure to the value of the goods being manufactured.

Customer is located in the country concerned and wishes to have a purpose designed ship constructed by a shipyard which is located in the same country. The ship will take 12 months to construct, and customer is willing to pay $105 million for the newly completed ship in 12 months’ time. However customer does not have the funds available to make instalment payments as the ship is constructed.

Bank is located overseas.

Customer and Bank agree that Bank will construct the ship (or procure its construction) over the next 12 months and that once the ship is finished customer will pay $105 million to Bank for the completed ship.

Shipbuilder is located in the same country as the customer and has a shipyard which is also located in the same country.

Bank enters into a second istisna contract, this time with Shipbuilder. Under that contract Shipbuilder will construct a ship for Bank while Bank will make specified stage payments to Shipbuilder totalling $100 million. In 12 months’ time the ship is finished. Bank takes ownership of the ship from Shipbuilder and sells the ship to Customer for a price of $105 million. Customer pays Bank $105 million.

“Istisna” is used specifically for a contract under which something is to be made at the request of the counterparty. Unlike salaam, there is no requirement to pay in full when the contract is made. The price and specification of the goods to be manufactured must be determined when the contract is entered into.

Taxation systems differ from country to country. However, most countries have systems of corporate and individual taxation that seek to tax profits from trading and investment income, while giving some form of deduction for financing costs in computing taxable income. Islamic finance presents a challenge for such tax systems, as they have generally been developed within a framework of conventional financial transactions. Furthermore, as will be seen from the above structures, Islamic finance often involves many more transactions than a conventional finance transaction that achieves the same economic results.

The taxable profits of the financier and of the recipient of the finance need to be determined. Ideally the taxable income of both parties should be the same, regardless of whether they have used a conventional financial transaction or an Islamic financial transaction, if the two transactions have identical economic characteristics. Unfortunately that may not be the case with certain tax systems.

One of the factors that distinguish tax systems from one another is the relative emphasis they each place on “form” and “substance.” In this context, “form” is used to describe putting significant emphasis upon the legal form of a transaction. In other words how is the transaction classified from a legal perspective? In contrast, “substance” is used to denote an approach of basing the tax treatment primarily upon the economic reality of a transaction.

Tax systems based entirely on “form” or entirely on “substance” do not exist. Instead, there is a spectrum, with countries combining the two elements in varying degrees. Furthermore, different parts of a country’s tax system may have distinct positions on the spectrum.

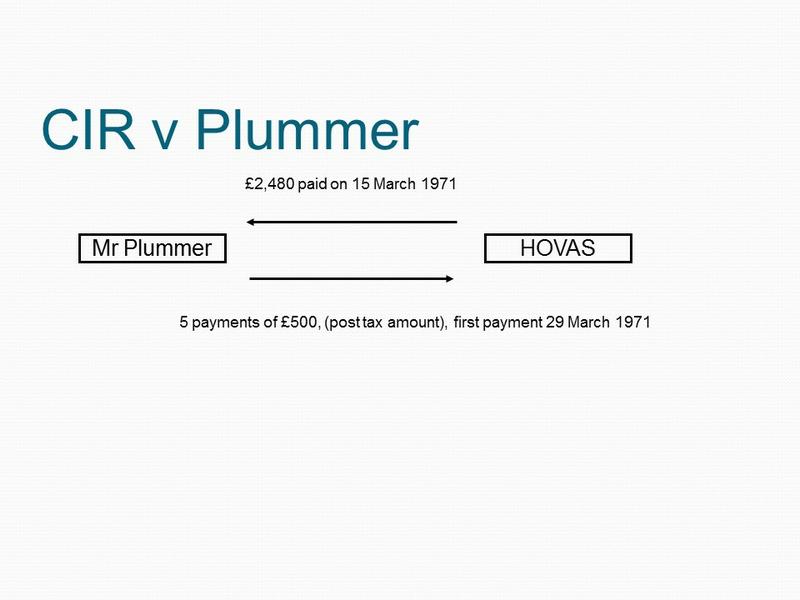

To illustrate the distinction between form and substance, it is helpful to review a UK tax case, Commissioners of Inland Revenue (CIR) V. Plummer, citation 54 Tax Cases 1. While the case was heard several decades ago, and its specific facts have been superseded by subsequent changes in UK tax law, it illustrates the form and substance distinction very clearly.

The facts of the case are relatively simple. On 15 March 1971 a charity called HOVAS paid £2,480 to Mr Plummer. In exchange, he undertook to make five annual payments to HOVAS under a deed of covenant, with the first payment due on 29 March 1971. The amount of each annual payment was whatever sum, after deduction of all taxes, amounted to £500.

The substance of the transaction was that Mr Plummer was borrowing £2,480 from HOVAS and repaying this in five annual instalments of £500; effectively borrowing at a relatively small rate of interest.

Under the legal form adopted, each of the £500 payments was treated as a larger gross payment from which Mr Plummer was entitled to withhold and retain income tax at the standard rate. For example, at the tax rate then prevailing, the first payment was legally a gross payment of £851.06. As a charity, HOVAS was entitled to a refund from the Inland Revenue of the tax withheld of £351.06, making the transaction very attractive to HOVAS; an internal rate of return of 27% was mentioned during the litigation.

Under the tax law then prevailing, Mr Plummer was entitled to offset the gross payment of £851.06 when computing his liability to higher rate tax, but not standard rate tax. The standard rate tax relief was already achieved by him deducting and retaining the £351.06. Accordingly, the transaction was also extremely attractive to Mr Plummer.

The tax authorities litigated and the case went through every level of the UK court system. Mr Plummer was successful before the Special Commissioners, before the High Court in 1977, before the Court of Appeal in 1978 (where the judges decided 3-0 in his favour) and before the House of Lords in 1979 (where the judges decided 3-2 in his favour).

The case is instructive to read as the legal arguments were directed almost entirely to the legal form of the transactions and whether the detailed stipulations of UK tax law had been complied with. The Inland Revenue did not attempt to argue that the transaction should simply be taxed on its economic substance as such an argument would find no support in UK tax law. (The courts might well take a different approach today, given the way case law has subsequently evolved in the UK.)

The author has surveyed how a number of Western countries treat certain Islamic finance transactions. It became clear that the closer a country’s tax system is towards the substance end of the spectrum (taxing the economic outcome), the less the specific adaptation needed to enable Islamic finance transactions to be conducted with the appropriate outcomes; namely that economic income is taxed and economic finance costs receive tax relief.

Conversely, tax systems based upon form, such as the UK, need specific legislation if taxable profit computations for parties engaging in Islamic finance are to be consistent with the economics of the transactions. That can be illustrated by looking at the commodity murabaha transaction above.

The customer’s loss of $5 is not an interest expense, since the contract involves no payment of interest. It arises from buying copper at an above market price ($105) and immediately selling the copper at the market price ($100). Under UK tax law this loss would not qualify as a trading loss, since entering into a transaction where there is no possibility of making a profit would not normally be regarded as trading. Consequently the customer would have no basis in UK tax law for deducting the $5 economic cost of obtaining the finance of $100 for one year. To ensure that the transaction could be carried out in the UK without such anomalous tax consequences, the UK enacted specific legislation for murabaha in Finance Act 2005 section 47. The tax law refers to the transaction as “purchase and resale.”

The sukuk structure above achieves the economics of a tradable bond, but entails two transfers of the building. That gives rise to a number of tax questions, some of which are listed below.

None of the potential tax costs mentioned in the questions above would be expected to arise if the equivalent conventional finance transaction (the issue by the Owner of a tradable bond secured on the building) had been entered into. If the tax costs do arise, the Islamic finance transaction is likely to be prohibitively expensive. As discussed below, the research found that countries differed in how well they had adapted their tax systems to enable such transactions.

Where transactions cross national boundaries, in many cases a foreign financier will engage in transactions involving assets located in a different country. In many cases, the transactions may be carried out either by representatives of the financier who are physically present within the country, or the customer may act as the financier’s agent for the purposes of the transactions.

For example, in the case of the commodity murabaha transaction, the Bank is purchasing the commodity from the commodity seller and then re-selling it to the Customer. Are these in-country transactions taxable? Does the Bank have a permanent establishment in that country by virtue of the activities of those who may be carrying out the commodity purchase and re-sale on its behalf?

Similar questions arise with regard to the salaam and istisna contracts.

The principles of international tax are relatively clear with regard to withholding tax from payments of interest. However they do not necessarily carry over easily to Islamic finance transactions.

In the case of the commodity murabaha transaction, when the Customer pays the Bank $105 after 12 months, this is legally the delayed payment of the $105 purchase price of the copper. Accordingly it is not immediately obvious whether the country of source can require any withholding tax to be deducted from the payment.

In the case of the ijarah sukuk, the income stream arises from renting the building, and countries often have different tax regimes for the payment of rent and the payment of interest. Accordingly can the country of source require the Owner to deduct withholding tax when paying the annual $5 million rent to the SPV? The SPV is offshore in this example, but if it were onshore, would it have an obligation to deduct withholding tax when paying income to the sukuk investors?

Most tax treaties were negotiated without any reference to Islamic finance. Accordingly they tend to be silent about the subject. Accordingly, in many cases the treaty may not assist taxpayers engaged in Islamic finance transactions who suffer a withholding tax in the country of source. The treaty may not reduce the rate of withholding, and it is possible that sometimes the country of residence may sometimes resist giving a credit for the tax withheld by the source country.

Furthermore the treaty definition of a permanent establishment may not assist a foreign financier avoid having a taxable presence in the country if in-country transactions are carried out on its behalf by agents located within the country.

The 2012 survey received responses from eight MENA countries: Egypt, Jordan, Kuwait, Libya, Oman, Qatar, Saudi Arabia, and Turkey. It also received a response from the Qatar Financial Centre, which is not a country but which has a separate set of tax laws applicable to the QFC.

The survey also included Malaysia, to provide a non-MENA comparator country, chosen because Malaysia has long been a pioneer in the development of Islamic finance.

The United Kingdom also provided a comparator country via the author’s detailed knowledge of the UK tax system. The UK was chosen because it is the leading non-Muslim majority country in Islamic finance, and has extensively amended its tax law to facilitate Islamic finance.

Malaysia is a country roughly 60% of whose citizens are Muslims. Accordingly Islam has a special place in Malaysian society. For example while Malaysian commercial law is secular and owes much to English law, the personal law applicable to Malaysian Muslim citizens governing matters such as marriage, divorce and inheritance is Shariah as applied by Shariah qualified judges.

The approach that Malaysia has taken to the regulation of Islamic finance has been to enact specific legislation for Islamic finance such as:

Most importantly, subsection 16B (1) of the Central Bank of Malaysia Act 1958 creates a “Syariah [Shariah] Advisory Council” for the Malaysian Central Bank (Bank Negara Malaysia). The Shariah Advisory Boards of all Islamic banks in Malaysia are required to follow any rulings laid down by the Shariah Advisory Council of the Malaysian Central Bank. The Malaysian Stock Exchange similarly has its own Shariah Advisory Council.

Furthermore Islamic financial institutions in Malaysia are not permitted to offer Islamic financial products without first having that product approved by the appropriate regulatory body (such as the Central Bank or the Stock Exchange) which will follow the guidance of its Shariah Advisory Council. Accordingly in Malaysia there is never any doubt as to whether a product being offered is an Islamic financial product, since all Islamic financial products must be approved in advance.

That in turn made it practical to make relatively simple changes to tax law to provide equal treatment for Islamic finance. This is illustrated by the Malaysian response to the research questionnaire from which extracts are reproduced below. Where emphasis has been added, that has been done by the author.

The key point is that, because the Malaysian tax authorities can always be certain whether a transaction qualifies as Islamic finance, it has been relatively straightforward to amend tax law to give equal tax treatment.

For example, the transactions in the underlying asset that are needed to enable sukuk to be issued can simply be disregarded for tax purposes, and the payments to the sukuk investors treated as effectively being made by the company which caused the sukuk to be issued, namely the original Owner of the property. The comments below in italics are taken verbatim from the Malaysian response.

Such a transaction described above, where approved by an appropriate regulatory body, would be seen and treated as an ordinary conventional loan.

The relevant provisions are as follows:-

a) Income Tax Act, 1967 – Paragraph 2(7) & 2(8)

“2(7) Any reference in this Act to interest shall apply, mutatis mutandis, to gains or profits received and expenses incurred, in lieu of interest, in transactions conducted in accordance with the principles of Syariah.

2(8) Subject to subsection (7), any reference in this Act to the disposal of an asset or a lease shall exclude any disposal of an asset or lease by or to a person pursuant to a scheme of financing approved by the Central Bank, the Securities Commission, the Labuan Financial Services Authority or the Malaysia Co-operative Societies Commission as a scheme which is in accordance with the principles of Syariah where such disposal is strictly required for the purpose of complying with those principles but which will not be required in any other schemes of financing.”

b) Stamp Act, 1949 – Schedule II, Para (6) [Giving an exemption]

“An instrument executed pursuant to a scheme of financing approved by the Central Bank, the Labuan Financial Services Authority, the Malaysia Co-operative Societies Commission or the Securities Commission as a scheme which is in accordance with the principles of Syariah, where such instrument is an additional instrument strictly required for the purpose of compliance with those principles but which will not be required for any other schemes of financing”

Sukuk issuance based on the Ijarah principle is common in Malaysia. However, usually in practice, it is noted that the SPV is usually owned and established by the Owner instead of a separate/independent party/charity. Please refer to Q19 [response reproduced immediately below] for further information on SPV treatment.

However, under S60I of the Income Tax Act, 1967 where an SPV is specifically established for the issuance of Islamic securities.

S60I states that:

“… where a company establishes a special purpose vehicle solely for the issuance of Islamic securities, any source of the special purpose vehicle and any income from that source shall be treated as a source and income of that company and such company shall have the right to receive and utilise any proceeds derived from the issuance of such Islamic securities”

“The SPV is exempt from the responsibility of doing all acts and things required to be done under the Act”

“Islamic securities” means Islamic securities which adopt the principles of mudharabah, musyarakah, ijarah or istisna’ approved by the Securities Commission or Labuan Offshore Financial Services Authority”

Such Islamic financing structures are not common in Malaysia.

Where the financing structure is seen as an approved loan, repayment of the capital portion is not taxable. The $5 would be treated as interest payment and subject to 15% withholding tax.

Strictly speaking, there are no specific tax provisions for Istisna financing transactions. In Malaysia however, financing structures which are based on Syariah principles (e.g.mudharabah, musyarakah, ijarah or istisna) are accorded tax neutrality, subject to first obtaining approvals from regulatory bodies, such as the Bank Negara Malaysia, Securities Commission or Labuan Offshore Financial Services Authority.

Muslims are a small minority in the UK, being about 4% of the population. Despite having an established church, the UK generally maintains separation between church and state which leads to the following policy requirements:

Without the enactment of special tax law for Islamic finance, the transactions studied in this paper would encounter the same kind of prohibitive tax costs that they encounter in the MENA countries which responded to the study questionnaire. However any legislation that the UK introduced needed to be responsive to the policy considerations outlined above.

Accordingly the UK has taken a radically different approach to that taken in Malaysia. It began by analysing what transactions were carried out in common Islamic finance transactions. This research involved activities such as discussions with Islamic bankers and reading prospectuses from actual sukuk issues, many of which were supplied to the UK tax authorities by one of the report writers. After this research, it was possible to draft tax law which enabled transactions of the type carried out in Islamic finance, but using free-standing definitions which did not reference Islamic finance in any way.

This is best illustrated by two examples.

Finance Act (FA) 2005 section 47 introduced legislation for something called “Purchase and Resale.” As part of the UK’s tax law rewrite project, FA 2005 s.47 has been repealed, and the corporation tax version of the rewritten legislation is found in Corporation Tax Act (CTA) 2009 s.503 which is reproduced below:

503 Purchase and resale arrangements

(1) This section applies to arrangements if—

(a) they are entered into between two persons (“the first purchaser” and “the second purchaser”), one or both of whom are financial institutions, and

(b) under the arrangements—

(i) the first purchaser purchases an asset and sells it to the second purchaser,

(ii) the sale occurs immediately after the purchase or in the circumstances mentioned in subsection (2),

(iii) all or part of the second purchase price is not required to be paid until a date later than that of the sale,

(iv) the second purchase price exceeds the first purchase price, and

(v) the excess equates, in substance, to the return on an investment of money at interest.

(2) The circumstances are that—

(a) the first purchaser is a financial institution, and

(b) the asset referred to in subsection (1)(b)(i) was purchased by the first purchaser for the purpose of entering into arrangements within this section.

(3) In this section—

“the first purchase price” means the amount paid by the first purchaser in respect of the purchase, and

“the second purchase price” means the amount payable by the second purchaser in respect of the sale.

(4) This section is subject to section 508 (provision not at arm’s length: exclusion of arrangements from this section and sections 504 to 507).

Looking at the legislation above, it is easy to see that it is defining a murabaha transaction. However the definition does not require the transaction to be Shariah compliant. For example the definition would apply perfectly well even if a haram (prohibited) commodity such as whisky were the subject matter of the purchase and resale. Other parts of the tax law go on to specify what tax consequences arise for the two parties to the transaction; very briefly the difference between the purchase price and the sale price is treated for tax purposes as if it were interest.

This structure was first legislated in Finance Act 2007, and the rewritten version for corporation tax can now be found as CTA 2009 s.507 reproduced below.

507 Investment bond arrangements

(1) This section applies to arrangements if—

(a) they provide for one person (“the bond-holder”) to pay a sum of money (“the capital”) to another (“the bond-issuer”),

(b) they identify assets, or a class of assets, which the bond-issuer will acquire for the purpose of generating income or gains directly or indirectly (“the bond assets”),

(c) they specify a period at the end of which they cease to have effect (“the bond term”),

(d) the bond-issuer undertakes under the arrangements—

(i) to dispose at the end of the bond term of any bond assets which are still in the bond-issuer’s possession,

(ii) to make a repayment of the capital (“the redemption payment”) to the bond-holder during or at the end of the bond-term (whether or not in instalments), and

(iii) to pay to the bond-holder other payments on one or more occasions during or at the end of the bond term (“additional payments”),

(e) the amount of the additional payments does not exceed an amount which would be a reasonable commercial return on a loan of the capital,

(f) under the arrangements the bond-issuer undertakes to arrange for the management of the bond assets with a view to generating income sufficient to pay the redemption payment and additional payments,

(g) the bond-holder is able to transfer the rights under the arrangements to another person (who becomes the bond-holder because of the transfer),

(h) the arrangements are a listed security on a recognised stock exchange, and

(i) the arrangements are wholly or partly treated in accordance with international accounting standards as a financial liability of the bond-issuer, or would be if the bond-issuer applied those standards.

(2) For the purposes of subsection (1)—

(a) the bond-issuer may acquire bond assets before or after the arrangements take effect,

(b) the bond assets may be property of any kind, including rights in relation to property owned by someone other than the bond-issuer,

(c) the identification of the bond assets mentioned in subsection (1)(b) and the undertakings mentioned in subsection (1)(d) and (f) may (but need not) be described as, or accompanied by a document described as, a declaration of trust,

(d) a reference to the management of assets includes a reference to disposal,

(e) the bond-holder may (but need not) be entitled under the arrangements to terminate them, or participate in terminating them, before the end of the bond term,

(f) the amount of the additional payments may be—

(i) fixed at the beginning of the bond term,

(ii) determined wholly or partly by reference to the value of or income generated by the bond assets, or

(iii) determined in some other way,

(g) if the amount of the additional payments is not fixed at the beginning of the bond term, the reference in subsection (1)(e) to the amount of the additional payments is a reference to the maximum amount of the additional payments,

(h) the amount of the redemption payment may (but need not) be subject to reduction in the event of a fall in the value of the bond assets or in the rate of income generated by them, and

(i) entitlement to the redemption payment may (but need not) be capable of being satisfied (whether or not at the option of the bond-issuer or the bond-holder) by the issue or transfer of shares or other securities.

(3) This section is subject to section 508.

It can be seen that the above section contemplates a sukuk transaction, with the following roles:

Other parts of the legislation, not reproduced here, have the effect that, provided the structure will not last longer than 10 years and various other specified conditions are met, the sale of the property from the Owner to the SPV and from the SPV back to the Owner is effectively disregarded for the purposes of corporation tax, stamp duty land tax (the UK’s real estate transfer tax) and capital allowances (the UK’s rules for computing tax depreciation.)

The UK has also amended its definition of a permanent establishment to ensure that foreign persons conducting in Islamic finance transactions within the UK are not thereby deemed to have a permanent establishment. The statutory definition of a permanent establishment is contained in Finance Act 2003 section 148 and a new section 5B has been added:

(5B) Where profit share return is paid, in accordance with arrangements to which section 49A of FA 2005 applies (alternative finance arrangements: profit share agency), to a company that is not resident in the United Kingdom, the company is not regarded as having a permanent establishment in the United Kingdom merely by virtue of anything done for the purposes of the arrangements by the other party to the arrangements or by any other person acting for the company in relation to the arrangements.

The UK’s approach requires the writing of far more legislation than the Malaysian approach, because the transactions have to be defined in meticulous free-standing detail, without being able to reference any definitions from elsewhere, and without being able to rely upon any form of advance certification of the structures by the regulatory authorities.

The philosophical approach in the UK is that private sector participants are free to enter into any contracts that they wish, apart from special cases where some contracts are prohibited by law or rendered unenforceable by law due to violating public policy as set out in English common law or occasionally due to violating specific legislative prohibitions.

The published report does not deal with double taxation treaties, which will be covered in Phase Two. However the author is aware that the UK has begun taking Islamic finance into account when negotiating treaties.

For example, the definition of interest in Article 11(2) of the current UK/US double taxation convention is as follows:

The term "interest" as used in this Article means income from debt-claims of every kind, whether or not secured by mortgage, and whether or not carrying a right to participate in the debtor's profits, and, in particular, income from government securities and income from bonds or debentures, including premiums or prizes attaching to such securities, bonds or debentures, and all other income that is subjected to the same taxation treatment as income from money lent by the taxation law of the Contracting State in which the income arises. Income dealt with in Article 10 (Dividends) of this Convention and penalty charges for late payment shall not be regarded as interest for the purposes of this Article. [Emphasis added by author.]

The highlighted text would deal with the profit from Islamic finance transactions which is taxed in the same way as interest is taxed. In the case of the UK the tax treatment is achieved by statute law, while in the case of the USA general principles should tax profits on an Islamic finance which are equivalent to interest in the same manner that interest is taxed.

The full reports summarises the response from each MENA country with regard to each of the four structures. However the responses can be condensed as follows.

None of the countries covered have modified their tax laws to facilitate Islamic finance, apart from Turkey which has introduced limited changes to facilitate the issue of sukuk where the SPV is located in Turkey and Qatar with its special tax regime in the QFC which contains specific provisions for Islamic finance.

For relatively simple Islamic finance transactions such as commodity murabaha, salaam or istisna, the application of the general tax laws of the countries concerned, unmodified for Islamic finance, appear to give results for the taxable income of the parties which broadly correspond with the results expected from an analysis of the transaction economics. However, depending on the details of the jurisdiction concerned, transaction taxes can arise which would not be payable in the case of a conventional finance transaction which had similar economic consequences. Furthermore some countries have problematical non-tax provisions; for example it was reported that Libya prohibits a foreign person buying a commodity in Libya and selling that to a Libyan person, as is done in the illustrative commodity murabaha transaction.

In the case of more complex transactions such as sukuk, the application of the general tax laws of the countries concerned, unmodified for Islamic finance, leads to prohibitive tax costs which can make the transaction wholly uneconomic to carry out. (Turkey is excluded from these comments as it has brought in special tax provisions to facilitate sukuk transactions.) These prohibitive tax costs arise from taxing the asset transactions associated with the issue of sukuk, even though these asset transactions ultimately reverse themselves leaving the asset with its original owner.

The report recommends that countries should modify their tax laws to facilitate Islamic finance, and contains different recommendations for Muslim majority and Muslim minority countries.

Religious issues can often cause difficulties in societies.

For example in the USA, during the global financial crisis, the insurance company AIG was bailed out by the US Government injecting emergency funds. Some of AIG’s subsidiaries had businesses, outside the USA, selling takaful (Islamic insurance) products. In the case Murray v. United States Department of Treasury, an individual filed suit against the US Government alleging that its injection of funds into AIG violated the First Amendment to the US Constitution since AIG was promoting a religion (Islam) through its takaful activities. The case was eventually thrown out by the courts on the grounds that the plaintiff lacked standing to bring the case although as of June 2012 the plaintiff was still seeking to appeal that decision. Subsequent research indicates that the appeal has not proceeded successfully and the case appears to be over.

The UK approach does not require any recognition of Islam within tax law, as the definitions of the transactions is entirely free-standing, and the desired tax treatment is given to all transactions that fall within the definition, regardless of whether they are Shariah compliant or not.

The principal drawback from following the UK model is that the legal drafting can take significant effort, since all aspects of the transaction must be described in meticulous detail without any reference to sources external to statute law.

As Malaysia has shown, amendment of the tax law to facilitate Islamic finance can be done relatively simply, if it is possible to be certain what is an approved Islamic finance transaction and what is not. Malaysia achieves such certainty by having a Shariah Advisory Council attached to each relevant regulatory authority such as the Central Bank and the Stock Exchange.

This approach requires far less complex drafting than does the UK approach. Accordingly, it will be much quicker to amend tax law to facilitate Islamic finance.

Central certification of Islamic financial products may at times slow down product development, but there should be advantages to customers from knowing that the product concerned has been approved as being Shariah compliant by the central regulatory authorities.

Some MNCs will not be able to have any involvement with Islamic finance because their businesses predominantly consist of activities that are prohibited by Shariah, such as gambling companies or alcohol producers. However large groups may contain subsidiaries that are separate legal entities which carry on permissible activities.

Firms which provide financial services may wish to provide Islamic financial services to Muslim customers who do not wish to consume conventional (the standard descriptor for "non-Islamic") financial services. Many larger financial services groups already have subsidiaries which provide Islamic financial services, but as the market grows there should remain scope for new entrants.

They should explore the feasibility of issuing sukuk from appropriate subsidiaries. This might provide funding that is cheaper the issuing conventional bonds, or give a marketing advantage.

Subject to assessments of cost when borrowing and credit risk when depositing, engaging with Islamic banks can broaden the commercial relationships of subsidiaries operating in Muslim majority countries.

The listed shares of many MNCs are potentially suitable investments for investors who follow the rules of Islamic finance. MNCs can make their shares more attractive to such investors by ensuring that they provide appropriate information disclosures within their financial statements, as additional information beyond the requirements of US GAAP or IFRS.

MNCs may be concerned that they lack sufficient knowledge of Islam. That is not necessary as the Islamic counterparties or advisors (in the case of sukuk issuance) will themselves bring with them the Shariah scholars who advise the counterparty. All that the MNC needs to do is to consider the financial merits of the transaction.

As revealed by the title, the published report envisages that the project will have later stages. Phase one concentrated entirely on direct tax and the four structures mentioned earlier.

Phase two, which is again being supported by the Qatar Financial Centre Authority, will look at two different topics:

It will look much more closely at the language used in double tax treaties, and make recommendations to those who negotiate double tax treaties and those who write official commentaries.

It will consider the theoretical issues Islamic finance presents for indirect tax systems. As well as looking at how selected jurisdictions have addressed those challenges, it will also make recommendations to those who create tax legislation.

Follow @Mohammed_Amin