Serious writing for

serious readers

Summary

Posted 10 November 2010

The text below was written in 2007 to form a chapter of the book "The Chancellor Guide to the Legal and Shari'a Aspects of Islamic Finance" edited by Humayon Dar.

I recently asked the publishers if they would be happy with me publishing my chapter here, and they consented. When reading it, please remember that the tax law is stated as of May 2007. Since then the tax law rewrite project has revised all of the statutory references, and there has been new legislation in the annual finance acts. However the broad understanding of the applicable tax rules that readers will gain remains generally valid.

Taxation systems differ from country to country. However, most countries have systems of corporate and individual taxation that seek to tax profits from trading and investment income, while giving some form of deduction for financing costs in computing taxable income.

Islamic finance presents a challenge for such tax systems, as they have generally been developed within a framework of conventional financial transactions. Accordingly, this chapter discusses some of the generic challenges that common Islamic finance transactions pose for tax systems. It then discusses how these challenges are being addressed by the UK. The UK is chosen both because of London’s leading position in international finance and because the UK is ahead of all major economies in adapting its tax system to facilitate Islamic finance. Accordingly, its example may be followed by other countries which have similar legal and taxation systems.

Advertisement

Click image

One of the factors that distinguish tax systems from one another is the relative emphasis they each place on “form” and “substance.” In this context, “form” is used to describe putting significant emphasis upon the legal form of a transaction, in other words how is the transaction classified from a legal perspective? In contrast, “substance” is used to denote an approach of basing the tax treatment primarily upon the economic reality of a transaction.

Tax systems based entirely on “form” or entirely on “substance” do not exist. Instead, there is a spectrum, with countries combining the two elements in varying degrees. Furthermore, different parts of a country’s tax system may have distinct positions on the spectrum.

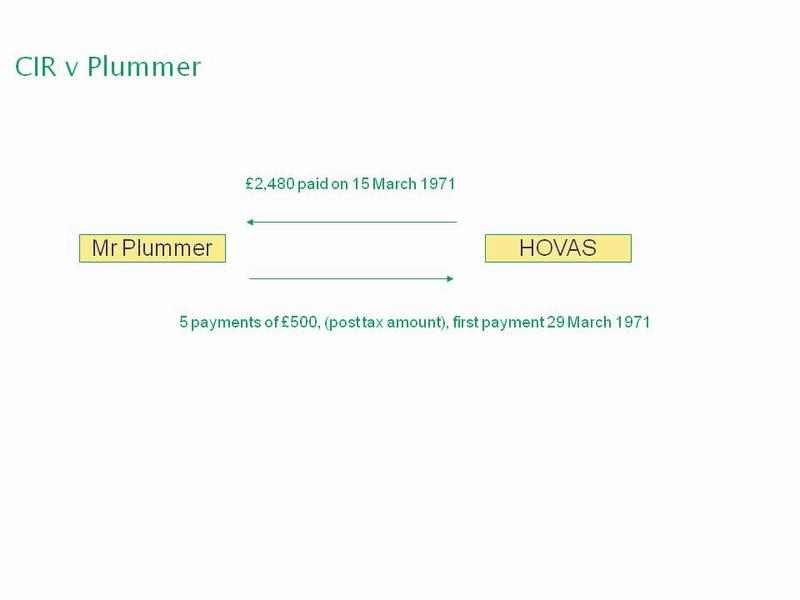

To illustrate the distinction between form and substance, it is helpful to review a UK tax case, Commissioners of Inland Revenue (CIR) V. Plummer, citation 54 Tax Cases 1. While the case was heard several decades ago, and its specific facts have been superseded by subsequent changes in UK tax law, it illustrates the form and substance distinction very clearly.

Diagram of the UK tax case Commissioners of Inland Revenue v Plummer

The facts of the case are relatively simple. On 15 March 1971 a charity called HOVAS paid £2,480 to Mr Plummer. In exchange, he undertook to make five annual payments to HOVAS under a deed of covenant, with the first payment due on 29 March 1971. The amount of each annual payment was whatever sum, after deduction of all taxes, amounted to £500.

The substance of the transaction was that Mr Plummer was borrowing £2,480 from HOVAS and repaying this in five annual instalments of £500; effectively borrowing at a relatively small rate of interest.

Under the legal form adopted, each of the £500 payments was treated as a larger gross payment from which Mr Plummer was entitled to withhold and retain income tax at the standard rate. For example, at the tax rate then prevailing, the first payment was legally a gross payment of £851.06. As a charity, HOVAS was entitled to a refund from the Inland Revenue of the tax withheld of £351.06, making the transaction very attractive to HOVAS; an internal rate of return of 27% was mentioned during the litigation.

Under the tax law then prevailing, Mr Plummer was entitled to offset the gross payment of £851.06 when computing his liability to higher rate tax, but not standard rate tax. The standard rate tax relief was already achieved by him deducting and retaining the £351.06. Accordingly, the transaction was also extremely attractive to Mr Plummer.

The tax authorities litigated and the case went through every level of the UK court system. Mr Plummer was successful before the Special Commissioners, before the High Court in 1977, before the Court of Appeal in 1978 (where the judges decided 3-0 in his favour) and before the House of Lords in 1979 (where the judges decided 3-2 in his favour).

The case is instructive to read as the legal arguments were directed almost entirely to the legal form of the transactions and whether the detailed stipulations of UK tax law had been complied with. The Inland Revenue did not attempt to argue that the transaction should simply be taxed on its economic substance as such an argument would find no support in UK tax law. (The courts might well take a different approach today, given the way case law has subsequently evolved in the UK.)

The author recently surveyed how a number of Western countries treat certain Islamic finance transactions. It became clear that the closer a country’s tax system is towards the substance end of the spectrum (taxing the economic outcome), the less the specific adaptation needed to enable Islamic finance transactions to be conducted with the appropriate outcomes; namely that economic income is taxed and economic finance costs receive tax relief.

Conversely, tax systems based upon form, such as the UK, need specific legislation. The distinction can be seen with some specific Islamic finance structures, as discussed below.

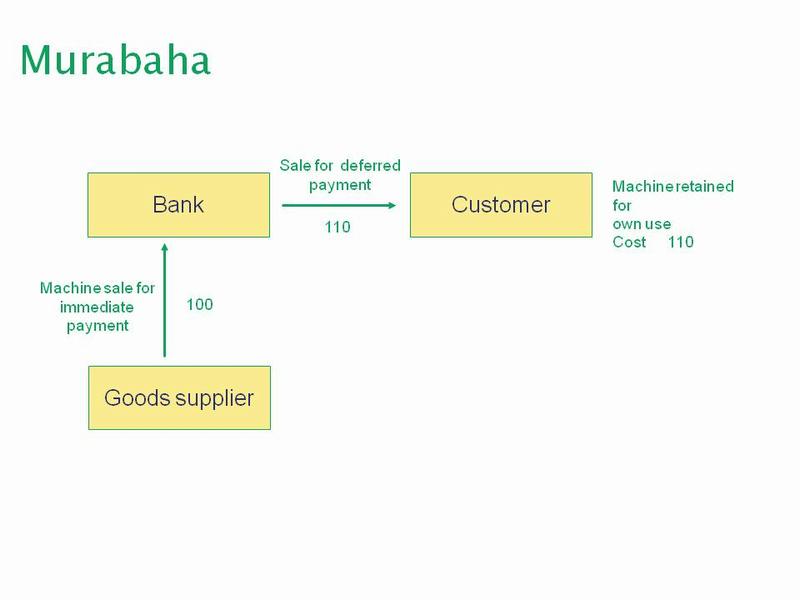

Diagram of a murabaha transaction

The above diagram illustrates a straightforward murabaha transaction. The customer wishes to have use of a machine but cannot afford the purchase price. Instead, a bank will buy that machine for, say, £100 and sell it to the customer for a price of £110, payable at some point in the future. The customer obtains immediate use of a machine worth £100, and has an obligation to pay £110 in, say, two years time. The extra £10 that the customer pays is clearly, in economic terms, the cost of the finance. However, the legal form of the transaction is that the customer is paying £110 to the bank to purchase the machine. From a taxation perspective, there are two alternative ways that the customer could be treated.

(a) The customer has contracted to pay £110 to purchase a machine.

That amount, £110, represents its cost and is the depreciable amount for tax purposes if the machine is eligible for tax depreciation. Accordingly, there is no separate recognition of the finance cost built into the transaction price. Instead, tax relief will be given over the life of the machine since the depreciable amount is £110 instead of the cash price of £100. Conversely, if the asset being purchased is not eligible for tax depreciation, then no tax relief will be obtained for the finance cost.

(b) The alternative approach is to decompose the transaction in accordance with the economic reality.

As the machine could have been purchased for £100 with payment being made immediately, the uplift in the purchase price of £10 in consideration of a two year deferral in payment is treated separately as a finance cost. Accordingly, the cost of the machine for tax depreciation purposes is recorded as £100. Meanwhile, the £10 finance cost is amortised over the two year deferral period obtained in exchange for this cost.

Murabaha transactions were one of the earliest forms used for Islamic property acquisition, as a replacement for conventional mortgages. However most countries have some form of real estate transfer tax. In the case of a conventional mortgage, real estate transfer tax is paid only once when the customer buys the property from a third party (whether using his own money or a bank mortgage). However, if a murabaha transaction is used there are two separate real estate acquisitions, one by the bank from the third-party selling the property and a second by the customer purchasing the property from the bank at a higher price. Accordingly, a murabaha transaction creates the very real possibility of double real estate transfer tax. This was the situation in the UK until specific legislation was enacted to abolish the double charge to facilitate Islamic property acquisitions.

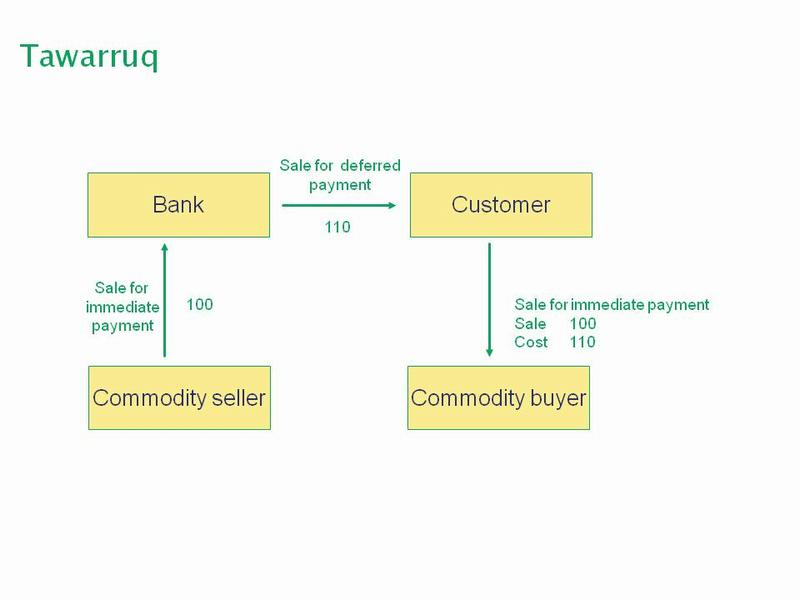

Diagram of a tawarruq or commodity murabaha transaction

In this case, the customer has a desire for cash which the bank wishes to provide without creating an interest bearing loan.

The bank will buy something that can be sold very easily afterwards, with little difference between the bid/offer (buy/sell) prices. A typical example would be a quantity of copper bought on a commodity market. The bank buys the copper, immediately paying £100 for it, and transfers ownership to the customer at a price of £110 payable in, say, two years time.

The customer can then immediately sell the copper for a price of about £100. This gives him cash equal to what the bank has laid out, £100, and an obligation to pay the bank £110 in two years time. The extra £10 is in economic terms the cost of the finance.

The issue to be decided is whether the customer is entitled to a tax deduction. The customer has purchased an amount of copper at a price of £110 payable in two years time, and sold that copper for £100 with the price being payable immediately. Accordingly, the customer has suffered a loss of £10. Is this loss tax deductible? The answer is not self evident.

If the tax system of the country concerned decomposes the transaction into its economic substance, then it is clear that the customer has obtained the immediate use of £100 in exchange for the obligation to pay £110 in two years time. That extra £10 would then be treated as a finance cost and tax deductible if an equivalent payment of interest would have been tax deductible. (Many countries have limitations on the circumstances in which interest expenses are tax deductible, which are beyond the scope of this chapter. Instead, the goal is to examine whether a cost of Islamic finance obtains equivalent tax treatment to conventional finance used in the same circumstances.)

However, the tax systems of some countries will not decompose the transaction as analysed above. The legal form is that the customer has actually purchased an amount of copper at a price of £110 and then sold that copper, for immediate payment, at a price of £100. Accordingly, its loss has arisen on the purchase and resale of copper.

Such a loss on the purchase and resale of a commodity may not be tax deductible. In the UK, for example, unless the customer can show that it is trading (as understood by tax law) in copper, it will not be entitled to deduct the £10 loss against its other income. Furthermore, even if the customer regularly trades in copper, this transaction does not look like a legitimate trading transaction since the customer knew that it would suffer a £10 loss when it commenced the transaction. (Trading is normally done with a view to profit.) Accordingly, under UK tax law (before the recent changes to facilitate Islamic finance), the customer would not be expected to obtain tax relief for its £10 cost.

For both murabaha and tawarruq one also needs to consider transaction costs such as transfer taxes. However detailed analysis is beyond the scope of this chapter.

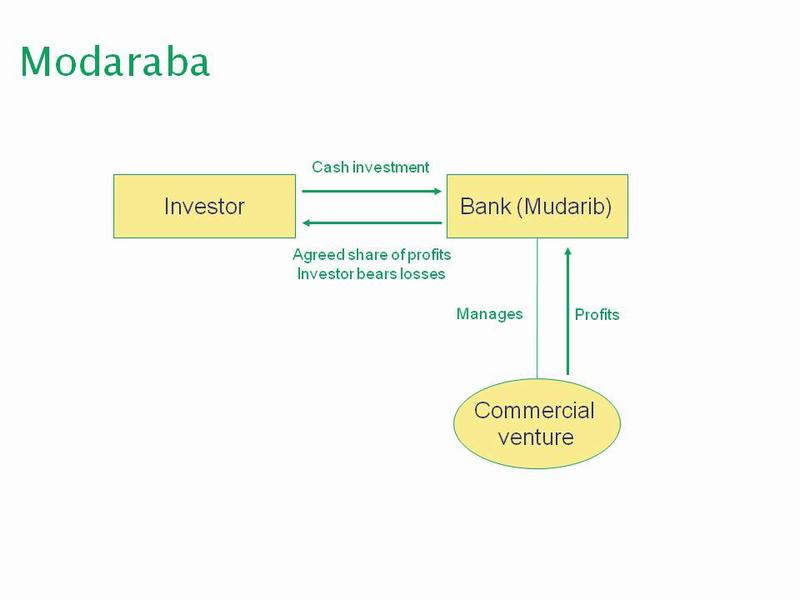

Islamic banks typically offer two distinct forms of accounts: current accounts, which are repayable in full but which give the investor no economic return, and savings accounts, which at least conceptually are exposed to the risk of loss but where the customer participates in the profits made by the bank from the use of the customer's money.

One such form of savings account is a modaraba deposit. This is illustrated in the following diagram.

Diagram of a modaraba transaction

In a modaraba transaction, the investor (the depositor in the bank) provides cash to the bank (acting as mudarib) to invest that money in a commercial venture, with the bank as mudarib managing that commercial venture. Typically, in the case of a bank the commercial venture will consist of the full range of its operating assets, both loans (transacted in Islamic form) to customers and financial assets held in the bank's treasury operations to ensure that the bank has sufficiently liquidity to repay its current account and savings accounts customers when required.

If there are profits from the bank’s operations, those profits are shared between the bank and the customer on an agreed basis. Typically, the customer obtains a return similar to market interest rates while the bank keeps any excess return as a reward for organising the transactions.

Most tax systems would be expected to tax the investor on the profits paid to it. Similarly, one would expect the bank to be taxed on all the profits that it makes from its operations while receiving a deduction for the profit sharing payments that it makes to its customers.

However, many countries such as the UK have very detailed tax laws. For example, the UK has always been concerned that parties providing finance may disguise what is in substance equity finance as debt to obtain the benefit of a tax deduction for interest. Accordingly, one of the many specific provisions regarding interest in the UK tax code is section 209(2)(e)(iii) of the Income and Corporation Taxes Act (ICTA) 1988. This applies to interest paid on “securities under which the consideration given… is… dependent on the results of the company’s business.” The effect is that the interest paid is treated as a distribution, in other words as a company dividend which means that it is not tax deductible. In the absence of specific legislation, this provision would most likely apply to the profit-sharing payments which the bank makes to its customer under the modaraba contract.

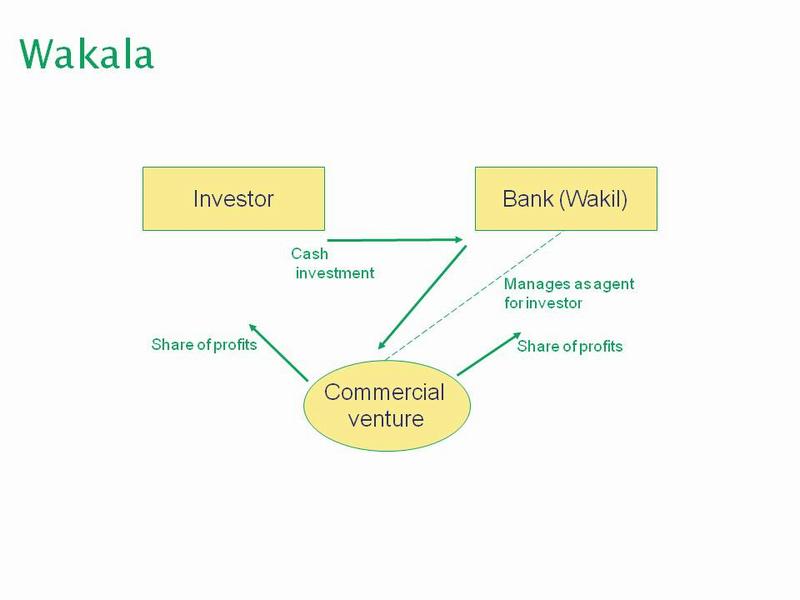

Another form of contract which can be used for an investor to provide money to a bank to earn an economic return is a wakala contract.

Diagram of a wakala transaction

In wakala, as with modaraba, cash is going from the customer as an investor and is used to finance a commercial venture with the profits of the commercial venture being shared between the investor and the bank (the wakil) in agreed proportions.

In this context, the key difference between wakala and modaraba is the legal relationship. In the modaraba contract referred to above, the bank borrows the cash investment from the customer and becomes legally indebted to the customer so that the legal form of the contract is that of a deposit. Conversely in wakala it is assumed that the bank (the wakil) is legally acting as an agent for the customer, so the money never becomes the bank’s property.

That distinction will matter in the event of the bank’s insolvency. In a modaraba contract, if a bank has taken what is a deposit at law and then becomes insolvent, the investor is limited to claiming in the bank’s insolvency along with its other creditors. With a wakala contract, if the agent bank becomes insolvent the investor should have a direct legal claim on the underlying commercial venture.

While this chapter draws the above clear distinction between a modaraba contract and a wakala contract, the distinction may not be so clear in practice. For example, the bank's standard wakala contract may permit the bank to commingle the customer's funds with those of other customers, making it impossible for a customer to trace his funds in the event of the bank's insolvency. If so, the customer will not have any stronger protection from the bank’s insolvency in the case of a wakala contract than with a modaraba contract.

The role of the bank in acting as agent for the customer may have significant consequences in international transactions. The approach of many countries is not to tax foreign persons unless they have a taxable presence within the country in the form of a "permanent establishment." However, the bank acting as agent for the customer in providing funds to the underlying commercial venture may be sufficient to cause the customer to have a permanent establishment within that country since the bank as agent is taking commercial decisions on the customer's behalf. The consequence may be to make the customer taxable on the profit paid to it whereas interest paid on a conventional bank deposit to a foreign person may not have been taxed by that country, either due to the country's domestic tax law or because many double taxation treaties give exclusive taxing rights on interest to the country where the customer is resident rather than to the country of source. Accordingly, replacing a conventional deposit with a wakala contract gives a risk of creating a taxable presence in the country where the bank is located.

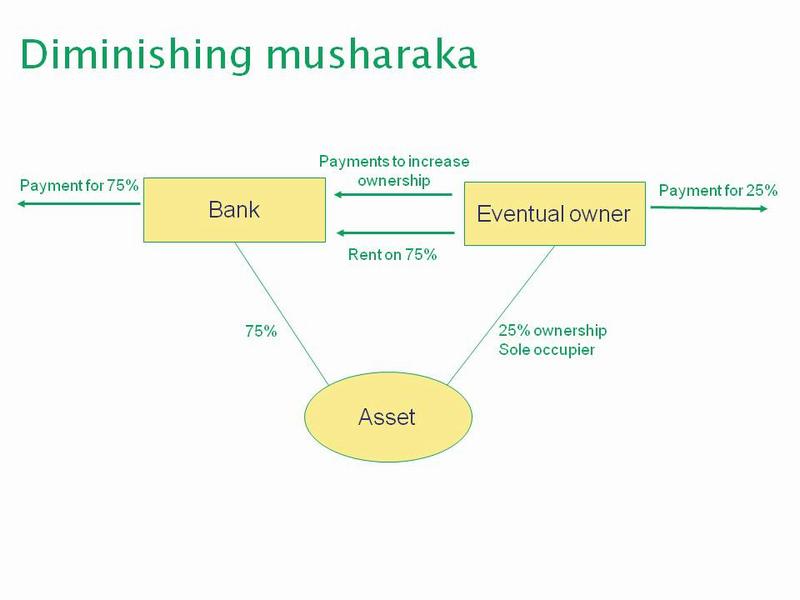

This is often used for people buying houses for owner occupation instead of a conventional mortgage, but can also be used for the purchase of investment property. It is illustrated in the following diagram.

Diagram of a diminshing musharaka transaction

Diminishing musharaka is used when one party, here called the eventual owner, wants to buy an asset but cannot afford to pay for all of it. In the diagram, on day one the bank buys 75% of the asset, for example a building, while the eventual owner buys 25%. Under the contract between the eventual owner and the bank, the eventual owner has immediate rights to sole occupation.

The eventual owner pays rent to the bank on the 75% of the property that it doesn’t own. Then, over the life of the arrangement, as well as paying the rent, the eventual owner will make additional payments to the bank to purchase additional slices of the asset.

The price for the additional slices of the asset will be set out in the diminishing musharaka agreement. While any price formula can be used, in practice two arrangements are most common:

At first sight, one would expect the eventual owner to receive tax relief for the rent that it is paying to the bank. This rent is being paid to enable the eventual owner to occupy the whole of the building even though it only owns 25% initially.

However, upon a closer analysis, tax relief for the whole rent is not entirely certain. This is because the eventual owner also has the right to purchase the bank’s share of the property over an extended time period.

If the purchase of additional slices will be at market value, then the rent that the eventual owner is paying does no more than entitle it to occupy the property. The level of the rent is likely to be the same as the rent that is paid in conventional property rental transactions where there is no intention for the tenant to purchase the property. Accordingly, in this scenario the entire rent should be tax deductible.

The analysis is different if the eventual owner is entitled to purchase of the bank’s share of the property at a price equal to the original price paid by the bank. In this situation, the rent paid by the eventual owner actually achieves two things:

This preservation of the entitlement to purchase at original cost has the nature of the payment for an option to the purchase of the building, rather than being a payment for the right to occupy the building. This can be demonstrated by considering the amount of the rent: one would expect this to be higher than the level that would be paid by a conventional tenant merely for the occupation of the property, as the eventual owner has greater rights than would a conventional tenant. Logically this additional element of the rent should be denied tax relief as being linked with the entitlement to purchase the property at the bank's original cost.

Banks which lend money on conventional mortgages often manage their balance sheets by securitising the mortgages. The normal approach is for the bank to sell the mortgages to a special purpose vehicle which finances the acquisition by issuing bonds to investors. Such securitisation transactions with conventional mortgages typically involve little or no transaction taxes.

However, consider the position of a bank which has entered into a number of diminishing musharaka transactions. If it wishes to transfer these transactions to a special purpose vehicle, it will most probably be involved in real estate transfers as the bank's participation in a diminishing musharaka contract involves the bank owning the property. Accordingly, securitisation potentially involves a further charge to real estate transfer tax.

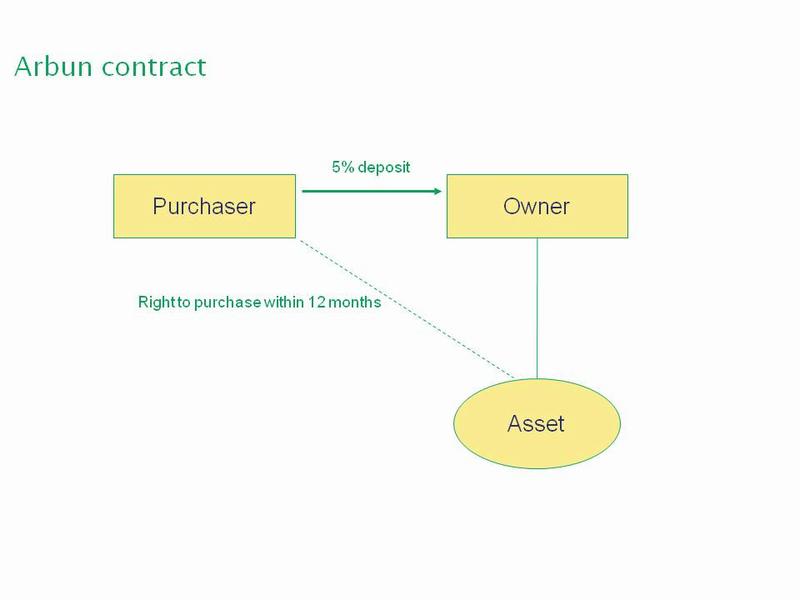

An arbun contract has the effect of replicating a call option.

Diagram of an arbun contract

In this example, the purchaser enters into a contract with the owner for the purchase of the asset, with the transaction to be completed at any time within the next 12 months at the election of the purchaser. A deposit is paid, in this example 5%, but the purchaser also has the right to withdraw from the purchase transaction albeit then forfeiting the deposit.

In economic terms, the transaction is no different from a call option with the deposit being equivalent to the option premium. However, it raises the question of how the owner is treated for tax purposes when entering into the contract for the sale of the property. At its simplest, does the transaction fall to be taxed when the original contract is entered into or at some later stage when it becomes clear that the purchaser will not exercise its right to revoke the transaction?

The goal when structuring a sukuk is to replicate the characteristics of bonds without infringing the rules of Shariah. The most important requirement is that there must be no interest, which in turn means that there can be no legal debt involved.

The goal is to design an instrument which:

The manner in which these goals are achieved is most easily considered by looking at a couple of examples.

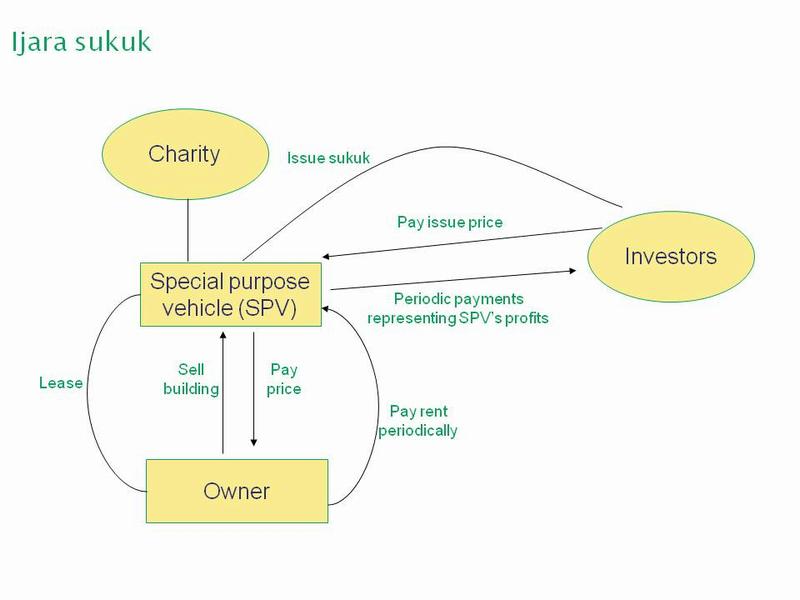

The diagram below illustrates how an ijara sukuk transaction would normally be arranged.

Diagram of an ijara sukuk transaction

The owner of a building wishes to use that building to raise finance. Accordingly, the owning company arranges for the creation of another company, typically a special purpose vehicle (SPV). This is a company which is not part of the owner company’s group; the shares of the SPV are normally held by a charity. The SPV raises the cash needed to purchase the building by issuing sukuk to the investors.

Legally, the sukuk are certificates which entitle the investors to a fractional share of the income that the SPV will receive from renting the building back to the owner. The SPV will normally declare itself as a trustee of the building on behalf of the sukuk investors, so that they have a beneficial entitlement to a proportionate share of the building and of the rent receivable from leasing it.

During the life of the sukuk, the owner will pay rent to the SPV which in turn will pay that money on to the investors. In economic terms, the investors have a prior claim on the profits generated by the owner from its business because part of those profits must be used to pay rent on the building to the SPV prior to any distribution of profits to the equity shareholders. However, this is achieved without creating a debt since leasing a building does not involve a debt claim.

At the end of the sukuk period, the owner will purchase the building back from the SPV and this provides the SPV with cash to repay the sukuk investors.

This transaction raises several potential taxation questions. Firstly, there are three land transactions, namely the original sale of the building to the SPV, the lease of the building by the SPV back to the original owner and finally the re-acquisition of the building by the owner. Each of these is potentially subject to real estate transfer tax or similar taxes on the leasing of land. Furthermore, the building may have appreciated in value between the original purchase by the owner and its sale to the SPV. Accordingly, the sale transaction may trigger a taxable capital gain.

When one considers the SPV, it is receiving rental income on the building which would normally be taxable. It then passes on that rental income to the sukuk holders who are therefore suffering taxation prior to receiving their cash. Conversely, if they had invested in conventional interest-bearing bonds, such bonds normally pay their interest gross without withholding tax.

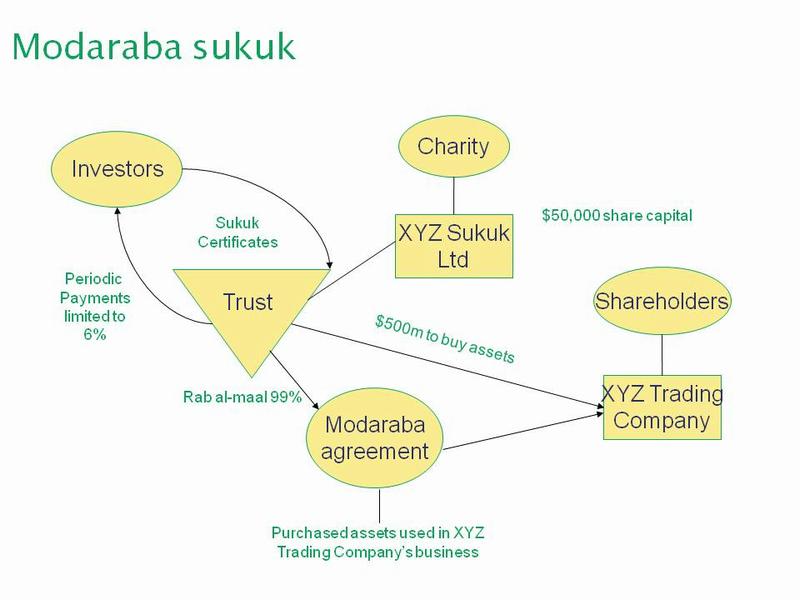

The diagram below shows how a particular modaraba sukuk was structured.

Diagram of a modaraba sukuk transaction

The sponsor was a company which had a collection of assets that were being used in its business. It wished to raise an additional $500m of finance. To achieve this, it set up the SPV, XYZ Sukuk Ltd, with share capital of $50,000. The SPV issued sukuk certificates to the investors for $500m and used the cash generated to purchase that amount of assets from XYZ Trading Company.

These assets were not rented back to the trading company, but instead used by the trust established by XYZ Sukuk Ltd to contribute, as “Rab al maal” (capital provider), to a modaraba agreement under which XYZ Trading Company would use the assets in its business, acting as mudarib. Nearly all (99%) of the profits generated from the use of these assets were to be paid to the trust, but subject to an overall limit of 6% of the investment (i.e. $30 million per year) which matched the maximum amount that would be payable on the sukuk certificates each year.

Through the medium of the sukuk and the modaraba agreement the investors have a prior claim to the profits being generated from the business, with that prior claim being limited to a maximum return of 6%. If the business generates no profits then nothing will be paid to the investors since there is no debt claim.

At the expiry of the sukuk period, XYZ Trading Company will repurchase the assets for $500m, allowing XYZ Sukuk Ltd to repay the sukuk certificates.

The above examples show how it is possible to replicate most of the economics of a debt instrument without infringing Shariah. In the ijara sukuk, the owner must pay the rent on the building in each period. Failure to pay the rent would result in eviction from the building, with the SPV then selling the building to a third party, and probably also suing the owner for non-payment of rent which could drive the owner into insolvency.

In the modaraba sukuk, the investors are taking a greater commercial risk. If the business activities conducted with the modaraba assets are unprofitable, there will be insufficient profit available to pay the investors their profit entitlement. Other things being equal, one would expect the maximum profit rate payable under the modaraba sukuk to exceed the rate of rent payable on the ijara sukuk, since the investors in the modaraba sukuk are in principle taking a greater degree of risk.

The modaraba sukuk structure outlined above raises several issues from a tax perspective.

(i) Potential treatment as partnership

Firstly the modaraba agreement looks very much like a partnership when analysed from a western tax and legal perspective. It is a basic principle of partnership taxation that distributions paid to a partner in respect of his profit entitlement are not tax deductible expenses. Accordingly, the 99% profit distribution to the Trust under the modaraba agreement looks as if it should be non tax deductible to the modaraba (partnership).

From XYZ Trading Company’s perspective, this may be less significant. If it had borrowed conventional debt, it would have been taxable on all of the profit from the business use of its assets, while obtaining a tax deduction for interest paid. Instead, with sukuk, part of the profit arising from using the assets would be taxable to the Trust (in its capacity of a participant in the modaraba partnership) and to that extent it would not be taxable to XYZ Trading Company.

However, when one considers the tax position of the Trust, one sees potential difficulties. The Trust would be taxable on its share of the income of the modaraba (partnership) as many countries will charge tax on partnership trading activities carried on within their territory, especially if the managing partner (here XYZ Trading Company) is resident within that country. This tax reduces the cash available to pay to the sukuk holders. After those sukuk holders receive their sukuk income payments, they may or may not be able to obtain a refund of the tax paid by the Trust or possible credit for that tax against taxes payable in their home jurisdiction.

The position is significantly unfavourable compared with the issue of a eurobond by XYZ Trading Company, where there would be straightforward tax relief to the borrowing company for the interest paid and no withholding tax on payments of interest to the eurobond investors.

(ii) Transaction taxes

As with the ijara sukuk, there is scope for transaction taxes when XYZ Trading Company (the sponsor) first sells the assets to XYZ Sukuk Ltd (acting as a trustee) and again when the sukuk expires as there will be a sale back of the assets to the sponsoring company.

As mentioned above, the UK is a pioneer among major western economies in adapting its tax law to facilitate Islamic finance. The government has had two strategic goals for making these changes.

The review of UK tax law in this chapter is based upon the law as it stood on 12 May 2007, assuming that Finance Bill 2007 is enacted as published but subject to any government amendments published prior to 12 May 2007.

The approach taken by the UK to set up a tax regime for Islamic finance is to enact specific legislation which sets out a definite tax treatment for certain specific types of Islamic finance, with economic returns equivalent to interest being treated in the same way as interest for all tax purposes. The new legislation is applicable to all financing arrangements which fall into its definitions, regardless of whether they are compliant with Shariah or not.

The legislation which is set out in Finance Act 2005 does not mention the Shariah or use any Islamic finance terms. Instead the legislation creates a freestanding set of definitions for use in UK tax law which are entirely neutral regarding religion. For transactions which fall within these definitions, the legislation specifies how to determine the finance cost and how that finance cost is treated by both the payer and the recipient. Broadly speaking, the finance cost is brought within the same tax rules as those that apply to interest.

The legislation does not change the nature of the financial arrangements, nor does it in any way impute interest, or deem interest to arise where there is none. It simply sets out a code for the tax treatment of transactions that fall within its definitions.

The legislation refers to two different types of finance cost:

This refers to the finance costs involved in murabaha and diminishing musharaka transactions. When the legislation in Finance Bill 2007 is enacted, it will also refer to the payments made to an investor in a sukuk.

This refers to the payments made to the investor in modaraba and wakala transactions.

The legislation begins with some introductory definitions, including that of a “financial institution” for the purposes of the legislation. “Financial institution” means—

(a) a bank as defined by ICTA 1988 s 840A;

(b) a building society within the meaning of the Building Societies Act 1986;

(c) a wholly-owned subsidiary of a bank within (a) or a building society within (b);

(d) a person authorised by a licence under the Consumer Credit Act 1974 Pt 3 (sections 21 - 42) to carry on a consumer credit business or consumer hire business within the meaning of that Act; or

(e) a person authorised in a jurisdiction outside the UK to receive deposits or other repayable funds from the public and to grant credits for its own account.

For the purposes of (c), a company is a wholly-owned subsidiary of a bank or building society (the parent) if it has no members except the parent and the parent’s wholly-owned subsidiaries or persons acting on behalf of the parent or the parent’s wholly-owned subsidiaries.

The ICTA 1988 s 840A definition of a bank is limited to UK and European Economic Area (EEA) regulated institutions. Accordingly (e) is needed to extend the definition of financial institution to non-UK authorised deposit takers. However, an equity capitalised company set up to provide Islamic finance but not licensed to take deposits would fail to meet the definition of a financial institution, and this may be a challenge for some non-UK Islamic financiers.

The requirement for bank or building society subsidiaries to be wholly-owned makes it relatively straightforward for bank groups to avoid these rules when desired, by having at least one share of the subsidiary owned by a person outside the group. The above reference to persons “acting on behalf of the parent” risks imprecision. For example, the question arises as to whether it would apply to the trustees of an employee benefit trust set up for the bank’s employees.

When Finance Bill 2007 is enacted, the legislation will apply to three types of contract that give rise to alternative finance return.

A finance arrangement can, as an alternative to payment of interest, be structured as a purchase of an asset and its onward sale at a higher deferred price. (This is discussed above under murabaha.) The provisions define the circumstances in which such a structure is to be taxed in the same way as if the return were a payment of interest. The difference between purchase price and sale price is treated as a “finance return”.

The following four conditions must be present for an arrangement involving a purchase and sale of an asset to fall within the provisions described here:

(a) a person (X) purchases an asset and sells it, either immediately or in circumstances in which the conditions described below are met, to the other person (Y);

(b) the amount payable by Y in respect of the sale is more than the amount paid by X in respect of the purchase;

(c) all or part of the sale price is deferred beyond the date of the sale; and

(d) the difference between the sale and purchase prices equates, in substance, to the return on an investment of money at interest.

The conditions referred to in (a) extend its scope where a financial institution holds a stock of assets for the purposes of a sale under an alternative finance arrangement.

Arrangements are excluded where neither party is a financial institution.

For the purposes of these rules, “the effective return” is the excess of the sale price over the purchase price of the asset. References to “alternative finance return” are to be read in accordance with the following rules:

(a) Where the sale price is paid on one day in full, the sale price is to be taken to include alternative finance return equal to the effective return.

(b) Where the sale price is paid by instalments, each instalment is to be taken to include alternative finance return equal to the “appropriate amount”.

The “appropriate amount”, in relation to any instalment, is an amount equal to the interest that would have been included in the instalment if:

(a) the effective return was the total interest payable on a loan by X to Y of an amount equal to the purchase price;

(b) the instalment were part repayment of the principal with interest; and

(c) the loan were made on arm’s length terms and accounted for under generally accepted accounting practice.

To clarify the main requirements, if Y is a financial institution, then X can be any person provided X sells the asset to Y as soon as X has purchased it; in the case of a non-immediate sale, irrespective of the status of Y, X must be a financial institution and must have bought the asset “for the purpose of entering into arrangements falling within” these provisions. The latter requirement could be problematic. For example, a car dealer wholly-owned by a bank has a stock of cars which it normally sells on hire purchase. If it purports to make a sale within these rules, it will fail to qualify as the stock was bought for other purposes. Instead, the car dealer could sell to another group company which then makes the alternative finance arrangements sale.

The requirement to apportion the effective return in accordance with generally accepted accounting practice (see above) should mean that a straight-line apportionment is unacceptable. However, this is not the case. HM Revenue & Customs (HMRC) in their published manual indicates that a straight-line apportionment would be accepted by HMRC, and there is no reason for a taxpayer to object to such acceptance. A strict actuarial apportionment is clearly acceptable and in most cases also an apportionment using the “rule of 78”.

As discussed above, this is often used as a Shariah compliant alternative to a mortgage. It requires arrangements under which both a financial institution and another person (called the eventual owner) acquire a beneficial interest in an asset. There are then a number of prescriptive requirements.

If the contract meets the statutory requirements, then payments by the eventual owner to the financial institution comprise alternative finance return, unless they are the payments for the acquisition by the eventual owner of the financial institution’s interest or payments for an arrangement fee, legal costs, or other expenses. For the avoidance of doubt, arrangements which qualify as diminishing shared ownership are expressly excluded from being a partnership for tax purposes.

Finance Bill 2007 contained eagerly anticipated provisions that enable UK companies to issue sukuk and clarify the tax treatment of UK resident investors buying and selling sukuk. The new rules will be inserted into FA 2005 and follow the consistent UK approach of precisely defining transactions in the tax statute and then applying the tax law, irrespective of whether the transactions are intended to be Shariah compliant or not.

There is a new definition of arrangements which give rise to an alternative finance investment bond. They require:

Having set out a prescriptive set of definitional requirements, the Finance Bill then contains a number of relaxations:

It is possible to designate a stock exchange for the purposes of the alternative finance investment bond rules, without having to designate it for other purposes. (This power may be used in future to designate certain foreign exchanges where existing sukuk are listed without the UK having to recognise those exchanges for all other tax purposes.)

A finance arrangement can, as an alternative to payment of interest, be structured as a person investing money on behalf of another with a view to making a profit which is shared between the two parties. (This was discussed above under modaraba and wakala.)

This is the second type of arrangements dealt with in the legislation. FA 2005 enacted the provisions for what is now called a “deposit” (essentially modaraba), while FA 2006 also introduced a new category, “profit share agency” (essentially “wakala”) by amending FA 2005.

In the legislation, “profit share return” means amounts paid or credited in respect of a deposit or in respect of a profit share agency, as detailed in the following provisions.

Under general tax rules (as discussed above), a payment of part of the profit to the investor would be treated as a distribution. The provisions define the circumstances in which such a structure will be taxed in the same way as if it involved payment of interest. Essentially, the arrangements will involve the sharing of profits between a customer and a financial institution in a form that represents a return on the customer’s deposit.

Subject to the rules covered below concerning provisions that are not at arm’s length, the following four conditions must be present for an arrangement involving a profit share payment to fall within the provisions described here:

(a) a person (the depositor) deposits money with a financial institution;

(b) the money, together with other money deposited with the institution by other persons, is used by the institution with a view to producing a profit;

(c) from time to time the institution makes or credits a payment to the depositor, in proportion to the amount deposited by him, out of any profit resulting from the use of the money; and

(d) the payments made or credited by the institution equate, in substance, to the return on an investment of money at interest.

The requirement in (d) could theoretically cause difficulty if the institution is very successful at producing profits and pays these to the depositors. For example, if the deposits taken were used to finance share dealing with profits of zero in some years and say 25 per cent in others, the question arises as to whether the bank’s payments would satisfy the condition. Assuming they do not, question then arises as to how one identifies the boundary. The problem may not arise in practice, as bank regulators are unlikely to authorise deposit contracts which expose the depositors to a meaningful risk of sharing trading losses, although that would be normal in a modaraba contract. The need to eliminate the risk of loss to depositors may significantly reduce the profits available for payment to them.

In the case of a profit share agency, the financial institution acts as agent of the principal (the investor) and uses the money provided by the agent with a view to producing a profit. Whereas in most principal/agent relationships the principal is entitled to most of the rewards (and risks), in the case of a profit share agency the principal is entitled to the profits to a specified extent while the agent is entitled to any additional profits (and may also be entitled to a fee). The provisions require the payments to the principal under his profit entitlement to equate, in substance, to the return on an investment of the money at interest.

If the above conditions are met, the amounts paid to the principal are a profit share return, while the principal is not taxable on the profits to which the agent is entitled.

The provisions regarding profit share agency inserted into FA 2005 by FA 2006 are, however, silent on the attribution for tax purposes of the profits of the underlying commercial venture undertaken by the agent with the money provided by the principal.

The profit share return paid to the principal by the agent financial institution is treated as if it were interest paid by the agent under a loan relationship. Accordingly, to reach the expected taxation answer, the agent needs to be taxable on the whole of the profit earned from the commercial venture. However, there seems to be a lacuna, in that the legislation apparently omits specifying that the financial institution shall be taxable on the whole of the underlying commercial profit which it produces in its capacity of agent. Instead, the agent financial institution seems to be left with a deduction for its payments to the principal, but with no amounts on which it is taxable. The draftsman may have assumed that the financial institution is taxable upon the whole of the underlying commercial profits from the venture on general principles, but such an assumption appears to ignore the fact that the financial institution is acting only as agent for its principal.

HMRC had never accepted that the FA 2006 profit share agency legislation contained the above defect. However to put the matter beyond any doubt, an amending provision is contained within Finance Bill 2007 to ensure that the profits of the underlying commercial venture are taxable upon the agent before giving a deduction for the amount paid to the principal.

The following general provisions apply both to contracts giving rise to alternative finance return and to contracts giving rise to profit share return.

Where a company is a party to an arrangement within the purchase and resale and diminishing shared ownership provisions described above, the loan relationships regime set out in FA 1996 has effect in relation to the arrangements as if:

(a) the arrangements were a loan relationship to which the company is a party;

(b) the amount of the purchase price of the asset were the amount of a loan made to the company by, or by the company to, the other party to the arrangements; and

(c) alternative finance return payable to or by the company under the arrangements was interest payable under that loan relationship.

Where a company is a party to a deposit arrangement within the provisions described above, the loan relationships regime has effect in relation to the arrangements as if:

(a) the arrangements were a loan relationship to which the company is a party;

(b) any amount deposited under the arrangements was the amount of a loan made by the depositor to the financial institution; and

(c) the profit share return payable to or by the company under the arrangements was interest payable under that loan relationship.

Similarly, in the case of a profit share agency the loan relationships regime regards the company as a party to a loan lent (if the company is the principal) or a loan borrowed (if the company is the agent).

The effect of applying the loan relationships provisions is to bring in all the detailed rules set out in FA 1996 which govern the treatment of debt and interest in UK tax law. This is accomplished by deeming loans and interest to exist for tax purposes; there is no implication in the tax law that the transactions give rise to debt for any other legal purposes.

Alternative finance return or profit share return is treated for income tax purposes in the same way as interest.

The rules for relief for interest against income tax in ICTA 1988 sections 353 - 368 are applied to alternative finance arrangements as if the arrangements were loans and the alternative finance return were interest. This includes the rules about certificates of interest paid.

The following rules apply where a person, other than, a company is a party to alternative finance arrangements for the purposes of a trade, profession or vocation carried on by him or a property business of his.

(1) Alternative finance return or profit share return paid by a person is to be treated as an expense of the trade, profession or vocation or of the property business.

(2) Incidental costs of an alternative finance arrangement qualify for tax relief on the same basis as incidental costs of finance by applying the rules in the Income Tax Trading and Other Income Act (ITTOIA) 2005 s 58 as if:

The provisions described here ensure that, where the parties to what would be an alternative financial arrangement are connected and the recipient of the alternative finance return is not subject to tax on that return, the arrangement is not treated as an alternative finance arrangement. They also deny any tax relief to the payer of the alternative finance return.

The provisions apply where:

Where the provisions apply, arrangements are not to be alternative finance arrangements. In such cases, the person paying relevant return is not entitled to any deduction in computing any profits or gains for the purposes of income tax or corporation tax, or against total income or total profits in respect of the relevant return. Where a deduction for relevant return is denied, group relief (which allows companies to surrender certain types of losses to other companies) is also denied.

This far-reaching provision may be regarded as part of HMRC’s new approach to international tax arbitrage.

If an arrangement falls within the definitions given above, then a number of significant tax consequences follow. It should be noted that these apply only for tax purposes, and not for other legal purposes.

The overall approach is that the rights of the bond holder (normally expressed in the form of sukuk certificates) are treated for tax purposes as if they were debt securities giving rise to interest income. This overall result is achieved by a number of detailed tax provisions including the following:

The definition of financial institution given previously is extended to include the issuer of an alternative finance investment bond, but only in relation to bond assets which are rights under arrangements falling within purchase and resale and diminishing shared ownership discussed above.

The new alternative finance investment bond rules will be particularly useful for Islamic banks seeking to securitise their portfolios of murabaha and diminishing musharaka assets by issuing sukuk, provided these assets fall within the definitions above for purchase and resale and diminishing shared ownership. However they appear insufficiently broadly drawn for the purpose of facilitating many other types of sukuk transactions. For example, they do not appear to assist a company seeking to implement an ijara sukuk using a UK building as discussed above.

To ensure that the effective return on arrangements (within the rules described above) is not taxed or relieved twice, the effective return is excluded in determining the consideration for the sale and purchase for all other tax purposes where an asset is sold by one party to the other under an arrangement within those rules. This does not override cases where any provision of the Tax Acts or the Taxation of Chargeable Gains Act 1992 provides for the consideration for a sale or purchase to be other than the actual consideration received.

The rules for deduction of tax at source in part 15 Income Tax Act 2007 (previously within ICTA 1988 s 349) are applied as if the alternative finance return or profit share return were interest. This creates an obligation to withhold income tax. Contractually, the customer’s payment under the arrangements for purchase and resale described above will be for the purchase of the asset. However, the effect of the provisions defining alternative finance return is to split that payment for tax purposes into two components, the capital element of the price and the part representing alternative finance return. The withholding of income tax can then be imposed by this rule.

The rules in chapter 2, part 15, Income Tax Act 2007 (previously within ICTA 1988 sections 477A and 480A – 482) which require a building society or a deposit taker to deduct tax from interest paid under a relevant deposit, are applied to relevant arrangements as if the relevant arrangement was a deposit and alternative finance return or profit share return was interest.

The legislation sets out how alternative finance return is calculated if the return is paid in a currency other than sterling. Where alternative finance return is paid in a foreign currency to or by a person other than a company - and in circumstances where it is not paid for the purposes of a trade, profession or vocation or property business - then the effective return and the appropriate amount (see above) in relation to that person are to be calculated in that currency and each payment of alternative finance return is to be translated into sterling at a spot rate of exchange for the day on which the payment is made.

Strictly speaking, this provision may be unnecessary for companies as the general requirement to use generally accepted accounting practice for loan relationships and trading profits should mean that the legislation does not need to prescribe how the calculations to convert from other currencies into sterling are to be performed.

The provisions defining “permanent establishment” in FA 2003 s148 are amended to ensure that where a non-resident company is party to an arrangement within the above provisions, the company is not treated as having a UK permanent establishment by virtue of anything done in relation to the arrangement. This amendment is necessary because otherwise the actions performed in the UK by the customer or by the financier’s agents could look like the creation of a UK permanent establishment of the financier. This is because they will involve the purchase and sale of assets which may be tangible goods located in the UK.

The provisions in FA 1995 s127 dealing with persons who are not treated as UK representatives are amended to ensure that where a person not resident in the UK is a party to an arrangement within the above provisions, neither the other party to the arrangement nor any other person acting for the non-resident in relation to the arrangement is regarded as the UK representative of the non-resident in relation to alternative finance return.

The HMRC manual points out that although alternative finance return is treated as interest for UK tax purposes, it may not be interest for the purpose of double taxation agreements or for the Interest and Royalties Directive (2003/49/EC).

In the case of double taxation agreements, the matter needs to be considered treaty by treaty.

Article 11(2) in the new UK/US treaty, includes a definition of interest as: “all other income that is subjected to the same taxation treatment as income from money lent by the taxation law of the Contracting State in which the income arises”. Accordingly, for this treaty the HMRC caution does not apply and alternative finance return would be treated as interest for the purposes of the treaty.

However, the Organisation for Economic Cooperation and Development (OECD) Model Treaty does not contain similar language and the HMRC caution appears appropriate. Having said that, in most cases alternative finance return should fall within Article 21 of the OECD Model Treaty (other income) and be taxable only in the country of residence, protecting the recipient from all UK withholding tax- even if the interest article of the treaty has a withholding rate above zero. For the UK to deny the application of Article 21, it would have to contend that alternative finance return is not of an income nature, despite the fact that UK domestic law treats it as income and imposes an income tax withholding. Such a contention appears difficult to sustain if challenged through the mutual agreement procedure of treaties based on the OECD model.

In the case of the Interest and Royalties Directive it is clear that the definition of interest in Article 2(a) does not extend to alternative finance return.

Where the return on arrangements within the profit share rules (described above) is taxed by this legislation, it is not regarded as a distribution under the rules that apply where an amount payable by a company in respect of a security depends on the results of that company’s business (see above). As explained above, without this provision the paying company would not be able to claim a deduction against corporation tax for payments made under these arrangements.

4.8.1.1 Profit share agency and non-residents

Where the principal is a non-resident company, the actions of the agent - or of any other party acting for the company in connection with the profit share agency - do not cause it to have a permanent establishment. Similarly, the agent is not treated as a UK representative of the principal.

The Treasury has been given extensive powers to amend the alternative finance arrangements provisions by statutory instrument (a legislative process which does not require an act of Parliament) to cater for other arrangements which in its opinion equate to loans, deposits or other transactions involving the payment of interest, but which achieve a similar effect without the payment of interest.

The UK has not considered it necessary so far to enact specific legislation to facilitate Islamic derivatives, such as the arbun transaction discussed above.

FA 2006 Sch 26 contains a complete and relatively complex code governing derivatives transactions entered into by companies. (Detailed discussion is beyond the scope of this chapter.) The rules in Sch 26 should apply as satisfactorily to arbun transactions as they do to conventional derivatives transactions.

There is also tax legislation, albeit simpler and less comprehensive than Sch 26, that applies to derivatives such as forward purchase contracts entered into by persons who are not companies. Again this should apply equally well to arbun transactions.

Stamp duty land tax (SDLT) was legislated in FA 2003, and is the name given to the UK's form of real estate transfer tax. When FA 2003 was enacted, it contained the UK's first tax provision to facilitate Islamic finance by eliminating the double charge to SDLT on Islamic mortgages (once when a bank purchases the property and again when the property is resold to the customer) provided specified qualifying conditions were met.

Originally, the relief only applied to acquisitions by individuals but FA 2006 extended the relief to acquisitions by all persons, so it also applies to acquisitions by companies and partnerships. The SDLT legislation presently uses a definition of "financial institution" which is narrower than used in the alternative finance arrangement rules. However, Finance Bill 2007 will harmonise the two sets of legislation so in future the SDLT rules will always use the definition of financial institution set out in FA 2005 for the alternative finance arrangement rules.

As discussed above, the taxation of Islamic finance is simpler to accommodate if a country's tax system is based upon taxing the economic reality of transactions. Such countries will decompose an Islamic finance transaction into its constituent parts to identify the component that represents a finance cost, and tax/relieve it accordingly. However, even in the case of such countries, transaction costs need careful consideration and there would be merit in pressing for specific legislation to facilitate Islamic finance for those countries where Islamic financiers wish to operate.

Where countries base their tax system primarily on the legal form of transactions, it is essential to bring in specific legislation to facilitate Islamic finance.

The UK is a pioneer in this area. While the legislation enacted over the last few years has enabled Islamic banks to operate in the UK, and will now enable the issue of some forms of sukuk by UK companies, further legislation will be needed to cater for the full range of transactions that Islamic financiers wish to implement.

Most fundamentally, the UK rules require one of the parties to an Islamic finance transaction to be a financial institution. There is no such requirement in the case of conventional finance, demonstrating how far the UK tax system will need to adapt before there is a completely level playing field between conventional finance and Islamic finance.

You can dowload a PDF version of the above text, including a table of contents.

When the text was published, slight changes were made for reasons of space and it was not possible to include all of the above diagrams. The publishers have generously supplied a PDF of the chapter as published, which can be downloaded. Please note that the file is 10 Mb in size.

Follow @Mohammed_Amin