Serious writing for

serious readers

Summary

3 April 2010

Despite having an established church, the UK generally maintains separation between church and state which leads to the following policy requirements:

Against this background, the UK Government has supported the development of Islamic finance in the UK for two principal reasons:

The UK Government has given a small amount of monetary support to Islamic finance for promotional activity. For example an arm of the Government, UK Trade & Investment, has spent money taking a pavilion at the World Islamic Banking Conference in Bahrain. However most of the UK Government’s support has come in the form of legislative changes, and by spreading a clear message that the UK has a supportive environment for Islamic finance.

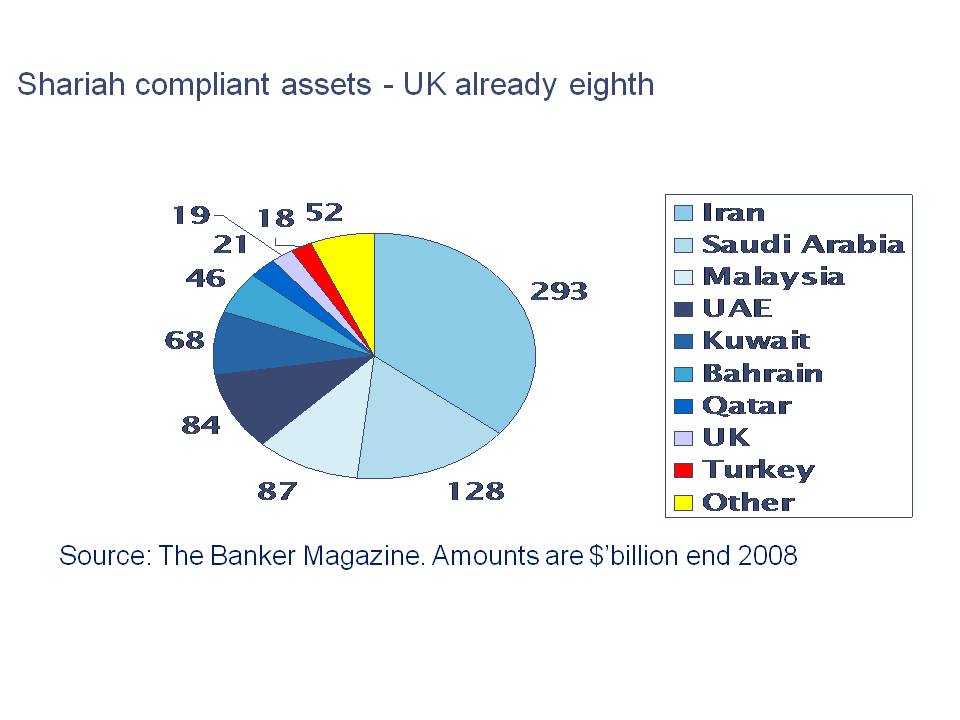

The success of the policy is most easily demonstrated by the size of the UK’s Shariah compliant banking and takaful assets. “The Banker” magazine has estimated that by the end of 2008 they were $19.4 billion, ranking the UK eighth in the world. This puts the UK ahead of such significant Muslim majority countries as Indonesia, Pakistan, Bangladesh and Turkey.

Almost all of the legislative effort has been directed towards ensuring that UK tax law treats Islamic finance no worse (and no better) than conventional finance. The tax law changes were needed because the UK tax system has grown over centuries in an environment where all finance was conventional finance. When Islamic finance began to be practiced in the UK, this created difficulties with respect to both transaction taxes and taxes on profits.

The issues are best explained by looking at finance for the acquisition of real estate.

Most real estate purchasers finance part of the price with a bank loan. The UK has a real estate transfer tax called Stamp Duty Land Tax (SDLT) which is paid on real estate purchases at varying rates up to a maximum rate after the March 2010 Budget of 5%. The purchaser pays SDLT on the entire purchase price when buying the property, but does not pay any more SDLT when any bank loan is repaid.

In contrast, an Islamic real estate purchase is often funded by a murabaha transaction or a diminishing musharaka transaction. In each case, the part of the property being financed by the bank is first purchased from the seller by the bank, and it will then be sold by the bank (either in one transaction or in stages) to the occupying purchaser. This involves two sales, and therefore two charges to SDLT.

The UK has eliminated the second charge to SDLT, provided various conditions are satisfied.

The UK began legislating in this area with the Finance Act (FA) 2005.

Strictly speaking, the UK has not enacted any Islamic finance legislation. A search of FA 2005 will fail to find words such as Islamic, Shariah, tawarruq or any other term used specifically in Islamic finance. The reason is that, as mentioned above, the tax treatment of a transaction cannot be allowed to depend upon whether it is Shariah compliant.

Instead, the UK identified certain types of transaction widely used in Islamic finance, and ensured that those types of transaction received appropriate tax treatment. This is illustrated by FA 2005 section 47 “Alternative finance arrangements”, reproduced here in full as originally legislated:

(1) Subject to subsection (3) and section 52, arrangements fall within this section if they are arrangements entered into between two persons under which—

(a) a person (“X”) purchases an asset and sells it, either immediately or in circumstances in which the conditions in subsection (2) are met, to the other person (“Y”),

(b) the amount payable by Y in respect of the sale (“the sale price”) is greater than the amount paid by X in respect of the purchase (“the purchase price”),

(c) all or part of the sale price is not required to be paid until a date later than that of the sale, and

(d) the difference between the sale price and the purchase price equates, in substance, to the return on an investment of money at interest.

(2) The conditions referred to in subsection (1)(a) are—

(a) that X is a financial institution, and

(b) that the asset referred to in that provision was purchased by X for the purpose of entering into arrangements falling within this section.

(3) Arrangements do not fall within this section unless at least one of the parties is a financial institution.

(4) For the purposes of this section “the effective return” is so much of the sale price as exceeds the purchase price.

(5) In this Chapter references to “alternative finance return” are to be read in accordance with subsections (6) and (7).

(6) If under arrangements falling within this section the whole of the sale price is paid on one day, that sale price is to be taken to include alternative finance return equal to the effective return.

(7) If under arrangements falling within this section the sale price is paid by instalments, each instalment is to be taken to include alternative finance return equal to the appropriate amount.

(8) The appropriate amount, in relation to any instalment, is an amount equal to the interest that would have been included in the instalment if—

(a) the effective return were the total interest payable on a loan by X to Y of an amount equal to the purchase price,

(b) the instalment were a part repayment of the principal with interest, and

(c) the loan were made on arm’s length terms and accounted for under generally accepted accounting practice.

Reading section 47, it is clear that it was designed to facilitate murabaha and tawarruq transactions. However it nowhere uses those terms and nothing in section 47 limits its application to Islamic finance. If a transaction falls within section 47, the tax treatment follows automatically, regardless of whether the transaction is (or was intended to be) Shariah compliant.

As mentioned above, the history of the UK tax system meant that it happened to contain specific provisions which would impact upon Islamic transactions, even though the equivalent conventional transaction was not affected. These were addressed by specific legislation.

For example, the UK has long had a provision to counter companies disguising equity finance in the form of debt, in order to obtain tax relief for payments that are economically equivalent to dividends to risk bearing shareholders. This can be found in ICTA 1988 s.209 (2) (e) (iii):

(2) In the Corporation Tax Acts “distribution”, in relation to any company, means …(e) any interest or other distribution out of assets of the company in respect of securities of the company (except so much, if any, of any such distribution as represents the principal thereby secured and except so much of any distribution as falls within paragraph (d) above), where the securities are …(iii) securities under which the consideration given by the company for the use of the principal secured is to any extent dependent on the results of the company’s business or any part of it.

This provision would preclude Islamic banks offering investment accounts to their customers, since the profit share paid to the customer would be treated as a distribution. This means that the payment would not be tax deductible for the bank. This problem was addressed specifically by FA 2005 s.54:

Profit share return [defined in FA 2005 section 49 in a form that corresponds to profit share return on investment account deposits of Islamic banks] is not to be treated by virtue of section 209(2)(e)(iii) of ICTA as being a distribution for the purposes of the Corporation Tax Acts.

This approach has successfully enabled Islamic finance to develop in the UK, without introducing religious issues into tax law or financial regulation. It could be copied by any country which wishes to promote Islamic finance.

Mohammed Amin

Follow @Mohammed_Amin